My cousin, Lt. Col. David Oclander, Battalion Commander, on the left.

As regular readers know, I’m a big fan of the National Association of Tax Professionals. They generally provide top-notch education, and I appreciate the fact that they do not discriminate against non-credentialed tax pros. Before I became a CPA, that was where I got most of my continuing education, because organizations like AICPA or NAEA are restricted to those with licenses. The IRS Tax Forums and web programming are more accessible, but often the quality of IRS presentation skills is pretty poor — they’re trained on compliance, not on public speaking. So when I see that NATP is hosting a class on an important topic that might not be getting enough promotion, I try to amplify it.

Today I’d love to highlight their upcoming session on August 29th: “Tax Planning for Military Personnel and Spouses“. NATP Instructor Mari Fries, EA, CFP explains that at the core of all military returns is the Servicemember’s Civil Relief Act (SCRA) and in more recent years the Military Spouse Residency Relief Act (MSRRA). Understanding the impact of these acts on a military return can result in thousands of dollars of tax savings for the service member and family.

I wanted to share it because I feel like this is a topic that doesn’t get much CPE time — it’s always a page in an update where the presenter says, “and I’m sure this doesn’t apply to anyone in here,” or “if this applies to your clients you already know the details, so I won’t go into it.” The most we can usually hope for is a link to the IRS webpage on Tax Information for Members of the Military or IRS Publication 3, Armed Forces Tax Guide. (To be fair, both of these are chock-full of great info, but it’s hard to suss out on your own, even as a professional preparer.)

If you have tax clients in the military, or you’re considering a niche in this under-served area, I strongly recommend this 100-minute, 2-CPE credit class. It will also be available on-demand.

From NATP:

At the core of all military returns is the Servicemember’s Civil Relief Act (SCRA) and in more recent years the Military Spouse Residency Relief Act (MSRRA). Understanding the impact of these acts on a military return can result in thousands of dollars of tax savings for the service member and family. This webinar, through case studies, will demonstrate the impact of these two federal laws on state returns and offer the preparer the knowledge necessary to identify when the SCRA and MSRRA are not being applied accurately at the state level. Additionally, we will cover other tax benefits afforded to our military personnel such as nontaxable pay and benefits, nontaxable combat pay and its impact on IRA contributions and EITC, and automatic extensions to name a few.

In this course, the instructor will teach you to distinguish between “home of record” and “domicile”, understand the impacts of the SCRA and the MSRRA on domicile, accurately identify when the laws are not being applied appropriately at the state level, and summarize special tax provisions available to military personnel.

Mari Fries, EA, CFP provides a preview of the course and her passion for the topic in this short YouTube spot:

According to the University of Florida IFAS Extension, there are a wide range of unique issues that affect tax filing for military families, including:

Moving expenses for permanent change of station (PCS) relocations

Sale of a primary residence or “accidental landlording” following a PCS move

Travel required for Reserve duty

Tax-exempt and taxable allowances (i.e., need-specific payments in military pay)

Tax-free “combat pay” for service in designated combat zones

Certain tax-filing extensions

Legal residency rules for state income tax filing (service members and spouses)

State tax rules for taxation of military retirement benefits

The opportunity to make tax-deductible pre-tax dollar (i.e., money that has not yet been taxed) contributions to the traditional Thrift Savings Plan (TSP)

A complete description of military-specific tax rules can be found in IRS Publication 3, Armed Forces Tax Guide. The IRS website also contains military tax tips and links to resources such as MilTax, a Department of Defense and Military OneSource program that provides free tax return preparation and e-filing for service members and some veterans, with no income limit.

Special congratulations to one of our cherished clients, Build Coffee, on being recognized by the City of Chicago as an essential part of their community, through nourishing food and a commitment to equity. Build Coffee is a coffee shop and bookstore in the Experimental Station on the South Side of Chicago. Surrounded by community-driven non-profits and civic journalism projects, Build is designed as a hub of great coffee and radical collaboration. They act as a small venue for performances, workshops, gallery shows, book groups, game nights, and more. They sell used books, local small press publications, journals, comics, art books, and zines. And they also run the Build Coffee Meal-Based Residency Program, a gallery show and residency aiming to nourish and sustain local art and artists.

News from the Chicago Department of Business Affairs and Consumer Protection (BACP):

Today, Mayor Brandon Johnson and the Chicago Department of Business Affairs and Consumer Protection (BACP) announced the grant awardees of the first round of the Good Food Fund Grant program. Forty-one Chicago food businesses were selected to receive a grant, fully funded by the American Rescue Plan Act, ranging from $10,000 to $100,000.

The goals of the Good Food Fund are to increase access to culturally relevant and nourishing food on the South and West sides, increase business ownership and jobs in the food industry, create stronger and more sustainable local food economies and increase local sourcing and supply of locally grown and regionally produced foods. The Good Food Fund programs, which are part of Mayor Johnson’s Road to Recovery Plan, were designed after intensive community engagement with the Food Equity Council and seek to help expand, enhance and restore the food industry using an equity and community-based approach. The second round of the Good Food Fund Grant application will launch on August 15, 2024.

“The Good Food Fund grant represents my commitment to equity and empowerment, ensuring every Chicagoan has access to fresh, local food,” said Mayor Brandon Johnson. “Congratulations to all food business grant awardees—your dedication to uplifting our communities through culinary innovation sets a remarkable example for us all.”

To ensure an equitable grant award selection process for all, the Food Equity Council and Allies for Community Business (A4CB), in collaboration with the City, assisted in developing the criteria for the Round 1 of the grant program. The goal was to provide businesses, across the food ecosystem, in communities with inequitable food access with an opportunity to apply for and receive a grant ranging from $10,000 to $100,000. Communities with inequitable access to food were determined using the Chicago Health Atlas.

“BACP is thrilled to collaborate with A4CB and the Food Equity Council on the Good Food Fund, a program designed to address food insecurity in underserved Chicago communities by providing customized food coaching, grants and access to low-interest loans,” said BACP Acting Commissioner Ivan Capifali. “By investing in initiatives that increase access to affordable food options, such as local growers, grocery stores and small food businesses, the City can empower its residents to make healthier choices and build more resilient communities.”

“Allies for Community Business believes that entrepreneurs from any background can start and grow businesses that create generational wealth for their families and communities,” said Brad McConnell, CEO of A4CB. “Through our partnership with the City and the Food Equity Council in administering the Good Food Fund and our joint venture partnership with ICNC at The Hatchery food incubator, we are excited to provide the grants, loans, coaching and kitchen space that entrepreneurs need to grow great businesses.”

Good Food Fund Grant Awardees:

Back of the Yards Coffee

Build Coffee

Carniceria La Hacienda

Carolyn’s Krisps

Chicago Eats Market Place

Chocolat Uzma

Contemporary Farmer

Dope Drip

Fatso Hard Kitchen

Give Me Some Sugah Bakery

Herban Produce

Jerk Soule

Jibarito’s y Mas South Side

Jus Sandwiches

Kabob-it

Ken Tone’s Drive-in

Kilwins Chocolate Fudge and Ice Cream (Hyde Park)

Kombuchade

La Esperanza

Let’s Eat to Live

Los Candiles Restaurant

Margaret’s Restaurant

Nary’s Grill & Pizza

Nicole’s Sandwich Shop

Nuevo Leon Bakery

Seafood Paradise on Jeffery

Shinju Sushi Japanese Restaurant

Spinzer Restaurant

Sputnik Coffee Company

Subway (Auburn Gresham)

Subway (Calumet Heights)

Supermercado Martin

SydPlayEat

Taquizas Y Banquetes El Siete

Taste Bud 1 Inc

Tatas Tacos

Taylormade Que

The Gilty Pig

The Jibarito Stop

The Tonk, Honky Tonk BBQ

Ware Ranch Steak House

A second round of the Good Food Fund Grant is scheduled to launch on August 15, 2024. An informational webinar will take place on Wednesday, August 14, 2024. To register for the webinar, please visit Chicago.gov/BACPwebinars.

To apply for the grant when it goes live on August 15, 2024, visit a4cb.org/grants. Entrepreneurs seeking grant application assistance can contact A4CB by calling 872-710-0035 or by sending an email to help@a4cb.org.

Good Food Fund business coaching and low-interest loans are currently still available through Allies for Community Business. Interested food entrepreneurs can contact A4CB at 312-275-3000 or schedule a consultation with a Business Coach or Community Lender at a4cb.loanwell.com.

✍️ Some of you may know that I’ve been writing this award-winning blog for 10 years now. Not monetized — just a labor of love that started out as a way to store articles for myself in an easy-to-search format. But during the pandemic its popularity exploded… not just for small business owners, but for the bookkeepers and accountants that keep them going. (If you didn’t already know my biggest passion is supporting small businesses & the communities that they help thrive and keep vital and colorful, then you must be new here.)

🔢 And I realized — when I help a small business, I help ONE of the key players in keeping local economies healthy. When I help a bookkeeper, I help a multiple of small business owners. When I help many bookkeepers… you can see where this is going…

🐣 Last year I decided that I wanted to focus my efforts on helping bookkeepers and tax pros learn to collaborate, and that the best way to start would be to offer a judgement-free space for bookkeepers to ask ANY QUESTIONS THEY WANT that for whatever reason they can’t ask their clients’ tax preparers (or, if in a firm, they don’t feel comfortable asking the tax department). And thus was born…

🏫 ASK A CPA! A member community designed to provide education, support, and resources for bookkeepers to better serve their clients — by preparing tax-ready books, improving relationships and building knowledge and systems that ultimately help small business owners and their communities.

❤️ We’re starting small, intentionally, and as such we’ll be capping our founding member group at only 50 people — there are only 9 spots left as of August 10th! Get in here and help us create the community you want to see in our industry. (Or feel free to just sign up for our updates if you want to have FOMO like all the time, that’s cool, too.)

All amazing things — any ONE of which would have made this the most incredible summer ever!

But I wanted to highlight this particular award from Bridging the Gap, as there are some special takeaways I’d love to share. First off, BTG is absolutely my favorite conference, and I’m delighted to announce that I’ve been invited to participate on their Advisory Board for 2025. (Why is it so special? Check out my LinkedIn post on the topic.)

Secondly, I feel like this award was an outward expression of the support and sense of community that I’ve been blessed to experience over the past many years — I’m so incredibly grateful to all who nominated me, especially the amazingly encouraging Melissa Miller Furgeson, who apparently rounded up many of the incredible members of my ‘Ask A CPA’ subscription, as well as the ‘Bookkeeping Buds’. And special gratitude to the team at BTG who voted, especially our beautiful and talented emcees Al-Nesha Jones & Nayo Carter-Gray, and our host, Randy Crabtree, for insisting that I belonged up there.

Bonus points: due to the space-theme of the BTG gala, I got to accept it while wearing a Jetsons dress.

I’m still floating through the clouds (quite literally, as I’m writing this from a window seat on the plane) on my way home from Scaling New Heights, where I was awarded Insightful Accountant’s 2024 Top Client Services ProAdvisor. And I’ve been thinking about how lucky I was to stumble into bookkeeping and accounting as a profession, and how much the support and education that QuickBooks provides to its ProAdvisors has played a part – not only in our team’s success, but also our clients’.

There are so many conferences, webinars, colleagues, apps, and tools that have helped me find this path, but unquestionably one of the most valuable has been our free subscription to the ultimate QBO client services tool – QuickBooks Online Accountant (QBOA). My team and I rely on its capabilities daily, and I can’t imagine running our practice without it. We reduce time spent on manual tasks, as well as review our clients’ books for accuracy and insights… basically a level-up on the already-robust basic subscription, with a version that’s designed for professionals who serve multiple clients.

Why does Intuit give us an accountant-specific bells-and-whistles version of QBO for free? Couldn’t they make a bunch of money selling this to us as an add-on? For sure… I see that angle, and I often worry they’ll switch to that approach someday. That’s how it was set up for QB Desktop – you had to pay to be a QBDT ProAdvisor, which gave you a special multi-client version of the software that allowed you to make edits and adjustments to client books and sync them between your system and theirs. But as you know… QBO already lets you do that, by the nature of its being cloud software-as-a-service, and so the extra bells-and-whistles aren’t as expensive to maintain as their Desktop counterparts. And having small business owners’ books prepared or reviewed by professional bookkeepers makes those businesses more likely to thrive, succeed… and remain in the Intuit ecosystem. It’s a win-win.

But I’m surprised at how many bookkeepers, even those who are already ProAdvisors, don’t realize how powerful a tool QBOA is. So I wanted to highlight my favorite things about it that I use all the freaking time.

Accessing all your clients’ books from one login

This may sound obvious if you’re a regular QBOA user, but honestly – how many other SAAS packages let you do this? We use countless apps and banks with our clients, and with the exception of a few (heaping blessings here onto Relay, Gusto, Guideline, Bookkeep, and Synder), we’re constantly having to log in and out of them when switching clients. QBOA lets you do this with one simple toggle. Side bonus: all our team members are associated with my account, so they can also have their own QBOA login (and therefore their own list of clients) if they’ve simultaneously got their own side-hustle or company, something common in our particular staffing set-up as well as with companies that co-firm.

ProAdvisor-specific training

I’m a huge fan of lifetime learning, and QBOA makes this easy. When I was on QB Desktop, I struggled to find training that was specific to bookkeepers working with multiple clients (rather than material that focused on end-users). In the QBOA portal, they suggest a personalized training path, provide self-paced study materials, videos, and links to live trainings. It also keeps track of your certifications and suggests new ones.

Client Overview

When doing a diagnostic review of a potential client, you should have them invite you as an accountant-user. Once that’s accepted, you can go into their books – and because of QBOA, you’ll have access to a Client Overview page, which gives you a sense of how much work it would take to bring them up-to-date, summarizing the most important points about banking activity, common issues, and transaction volume. For us, it’s an absolutely essential step that helps us determine whether we’re interested in working with the client, and if so… how much to charge for a clean-up and ongoing services.

Books Review ➡️ Transaction Review

Just below the Client Overview on the left-nav bar is an unassuming little item called “Books review”. Click into that and you’ll find a series of headers – the first of which, “Transaction review” is my favorite. It’s like QBOA is your junior accountant, digging through the books to find unaccepted bank feed transactions, uncategorized transactions, transactions without payees, undeposited funds, and unapplied payments. And it transports you to where you can actually fix a lot of these problems on behalf of the client (or you can give them a heads-up and ask them to DIY before you dig into your review). Until this feature was developed, we literally had folks combing through transactions – and there was no transparency into how bad things were in each area, which meant we didn’t know how long it would take us to go back-and-forth with the client to get things fixed… and this is before we even are taking care of reconciliations and reviews – truly foundational stuff that needs to be addressed right off the bat so that the books are in good-enough shape to address the big issues. I don’t want to use the phrase “game-changer” because it didn’t change the game… it moved us into a higher league of play.

Books Review ➡️ Account Reconciliation

Account reconciliation is the header just to the right of Transaction review, and it performs the next round of what we would normally ask a junior accountant to do – it shows the current status of each of the bank accounts, in terms of when they were most recently reconciled, as well as the number of and a list of unreconciled transactions. You can access reconciliation reports from here, look at the most recent statement if it’s in the system… and it doesn’t limit you to bank and credit card accounts; if you reconcile any of your Balance Sheet accounts, you can see this info, as well as link to them from here.

Accountant Tools ➡️ Reclassify Transactions

And what do you do once you’ve used Books Review to identify the myriad issues? This is where it gets really good, in my opinion. There are quite a few tools for accountants that are included in QBOA, but one in particular was a total game-changer when it was first released however-many years ago. And it’s just gotten better through the years. We have access to a tool called “Reclassify transactions” that our clients don’t get to use (just think of the mess they could end up making if they did). It allows us to filter transactions by type of financial statement or down to the specific account, and then also by date, type, and customer/ vendor. Once you’ve pulled up a list of all the transactions that fit your filters… you can reclassify or recategorize the ones you select. All at once. In a batch. You can even select just the ones that have a particular word in the memo (and with RightTool, another favorite tool, you can even filter by that word, or by a dollar amount or range)! It’s truly the most incredible feature, especially for cleanups. You can get quite granular with your filters and fix massive issues in a matter of minutes. Talk about a value-add.

Bonus! Chart of Accounts templates

I’m adding it as a bonus instead of one of the main features because it’s newish, so we haven’t yet had an opportunity to use it a ton – but I know it’s going to be a favorite. To be honest, this is one of those things that for years felt like it was just a missing feature; we used countless workarounds to standardize our clients’ Chart of Accounts, or at least make sure they all fit the format we use when preparing Tax-Ready Books (my passion and focus when providing education to bookkeepers). Intuit finally announced this feature at QB Connect last year and you should have heard the room burst into applause! The one trick to keep in mind is that you access the area where you build (or import, your choice) your templates from “Your Practice” as a QBOA user, not from each client. If you go to “Accountant Tools” while you’re in your ProAdvisor space, just after you log in – like where you’d go to get your Training – that’s where you see this option pop up in your toolbox. From there, you can get a video overview or take a guided tour. Once you’ve got your templates in there, you can assign them to a client or update their existing COA. Finally, wee-hoo!

And More…

There are other great features of QBOA that I know some of my colleagues adore – both ones that have been around for a while like reporting tools and app integrations, and newer ones like role-based access and permissions to clients’ books. But I meant to only list my top five and couldn’t do it under six, and then I wanted to add a bonus, and eventually this article will have to end or none of us will ever be able to get back to work and dive into the benefits QBOA offers. Enjoy!

Note! As my readers know, I am downright fanatical about transparency and full disclosure (often to my detriment, as you may have noticed that I have a wildly popular award-winning blog that is non-monetized). Though this particular post is a paid partnership with Intuit, I want you to know that a) I wanted to write an article on QBOA anyway, but couldn’t find the time; getting paid allowed me the break from client work I needed to make it happen; and b) they didn’t delete a single thing when I presented it. In fact, they have been totally cool with all my Intuit-bashing since the first article I wrote for them… which impressed me quite a bit, to be honest. That’s three times now — I might just keep this win-win-win up.

Thanks yet again, and as always, to Lisa Simpson from the AICPA Town Hall for her regular updates on what’s going on with Employee Retention Credit processing at the IRS. I can trust this team to make sure I’m getting the latest information, free from rumors and gossip, and that I’m able to both quell my clients’ concerns and also manage their expectations.

I had just been hearing some rumblings in one of my professional associations — someone had said, “seems inevitable that anyone who filed an ERC claim after September 2023 will need to file a lawsuit to get the claim paid,” and went on to suggest that it would be a great opportunity for a law firm, and wanted to know if we had referrals in this space.

First off, it made me nervous — our remaining ERC claims, all for deserving small business and non-profit clients of a colleague, worked really hard to make sure we had what we needed to submit their claims by January 31st, 2024, since there was pending legislation that might retroactively end the program after that date. They all were informed that it might be a year or more before they received the money, given the IRS moratorium — but certainly none of us expected to line the pockets of an attorney in order to get the claims paid out. And in fact, the claims were mostly small enough that my guess is most lawyers wouldn’t bother with them.

Secondly… it made me suspicious. On what basis was this guy saying a lawsuit would be “inevitable”? I attend every single AICPA Town Hall and hadn’t heard anyone suggest this. And what a sad thing to suggest it would be a “great opportunity” for a law firm — to specialize in making money off those desperate to finally receive what they and their accountants had already worked so hard to obtain.

As usual, I decided to quell those fears until the next AICPA Town Hall, and I’m so glad I did, as Lisa Simpson made ERC the first topic in her Technical Update. She explained the recent IRS news release that likely triggered the unfounded rumblings I was hearing, as well as referenced a new Journal of Accountancy article that delved deeper.

My takeaway was that: while 10-20% of claims are clearly fraudulent, and the IRS is in the process of denying them; and another 60-70% show an unacceptable level of risk and will be examined carefully — there are also between 10% and 20% of the claims show a low risk. The IRS “will begin judiciously processing” more of these claims, and, according to the release, expects some of these payments to be made later this summer.

To me, that’s all good news. It means they’re working through the piles and expediting the ones that have straightforward claims where the businesses played by the rules, processing the oldest ones first. The rest will be examined more critically, or in the case of blatant fraud, flat-out denied.

The one disappointing piece of information is that no claims submitted during the moratorium will be processed at this time. But at least we know the backlog is being cleared to make way for them. Since the moratorium was put in place, the IRS has received over 17,000 claims per week.

I’ve let my clients know that they shouldn’t budget for these dollars for at least another year, but that there’s no reason to presume they won’t eventually receive the claims that are due to them.

And yet again I learned that if something sounds sensational and suspicious… it might not be grounded in evidence and analysis. Rely only on your trusted advisors for the education and resources that will help you guide your small business clients. (And then provide links to those resources to the sensationalists who spread misinformation.)

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.

One of my favorite books when I was a kid was “Hail, Hail, Camp Timberwood,” about a girl who goes to summer camp for her first time. She’s standing around, feeling (and probably looking) uncomfortable as all the return campers are running around, hugging each other, excited to be reunited. All of a sudden, someone runs up to her and gives her a big hug and says how happy she is to see her again. After a moment of total confusion, the girl leans in and says, “Don’t worry – we don’t actually know each other. I was just feeling left out and figured I’d join ‘em.” The two of them become fast friends and go off hugging others who looked out of place and letting them in on the joke. Before you know it, the entire place was full of everyone running around hugging each other and laughing.

While I can’t say this is likely to happen exactly like that at the upcoming Scaling New Heights conference in Orlando, I also wouldn’t be that surprised if it did. There will be heaps of people reuniting for the first time since last year (check out my video blog about those amazing takeaways as well as my recent article for Insightful Accountant). But there will also be loads of first-timers attending, who are nervous and out of their element. Find the other wallflowers and go up to them – tell them it seemed like maybe they didn’t know anyone there, either, and do they want to eat lunch together or go to a vendor booth or grab a drink? You’ll be delighted and surprised at how many of these folks you’ll stay in touch with through the years. Remember, progressive accountants and bookkeepers such as the kind you’ll find at SNH – especially those who go year after year – are excited you’re there, and they want to help make your experience better. Introduce yourself to someone who looks like they “belong” and say that you’re new, and not sure where to begin. I am sure they’ll point you in the right direction, take you under their wing, or introduce you to someone who might be a great conference buddy.

For today’s blog post, I’m going to be that conference buddy, and share with you my Expert Tips for Attending Scaling New Heights 2024.

And Joe Woodard himself hosted one on Maximizing Your Experience at Scaling New Heights 2024 — catch the recording here, and they’ve kindly made the slides available for all attendees. Lots of great info on ’em — definitely worth the download.

Plan ahead, make a schedule, but be comfortable diverging from it; that way you don’t waste time figuring out what to do in the moment, but you also don’t miss the organic opportunities that arise.

Make a list of vendors you’d like to meet; they’re often very busy during open Exhibit Hall time; it might be helpful to set up a time with them to meet during a session when the Hall is less busy. Bring a list of questions you’d like to have answered. Narrow your scope… it’s impossible to visit everyone. Pick a few areas of interest, look into which vendors serve those areas, and focus on them.

Connect on social media with others who will be attending, whether it’s in a Facebook group like Woodard Group of the Americas or QB Community Live, LinkedIn, or other platform, you can always use #SNH24 to find out who you already know that might be going. Engage and make plans ahead of time.

Check with your sales reps and vendors for the tools you love best — whether you’re already using them or plan to implement this year — to see if they are hosting any customer dinners or get-togethers. Same with professional associations you might be considering joining, like Bookkeeping Buds, Realize, or Roundtable.

Tip Two — DOWNLOAD AND USE THE MOBILE APP

The training schedule on the Woodard website does a nice job of giving you a visual to see which sessions are held concurrently, and which are 50-minutes versus 100 or 120-minutes. It also lists the course objectives for each session, below the description, which the app does not. However, you can only register for a session using the app or the mobile app — not via the main website’s training schedule. (The Scaling New Heights website agenda/ training schedule and the SNH app do not sync with each other.)

If you still have the app on your phone from last year, it will work! You just have to click “JOIN” on the new conference. Otherwise, check out the slides below from Woodard for app instructions, as well as my friend Mariette Martinez’s how-to video for the mobile app.

It’s definitely helpful to the community if you register ahead-of-time for the classes that interest you (such as “The Tax-Ready Bookkeeper”, my session at 12 noon on Sunday, June 16th)! This is how they determine which rooms will be assigned for each one. If there’s a lot of interest in a particular topic, they’ll give it a bigger room, and that makes life easier for everyone.

You can’t “like” or “favorite” any of the other sessions at the same time, as is the case with some apps… you can only “register”, and only for one per time slot. However, you can export as many sessions as you like from either the app or web version of the app to your calendar, which could be a workaround if you’re interested in more than one and want to track them all.

The app won’t let you register if it’s full. But that doesn’t mean you shouldn’t try to attend anyway! Lines will form for the “sold-out” sessions, and they will let additional people in if there’s capacity, which there usually is – get there early to be near the front of the line. There is almost always extra room and I’ve rarely been turned away.

If you click on the session, it will show you the description, as well as speaker info. If you click on the speaker, it will show their bio and all the sessions they’re teaching at the conference, as well as a link to their website. This is a great way to research which instructors you’d like to hear.

Tip Three — PACK WISELY AND COMFORTABLY

Wear comfortable shoes – this is the largest Marriott in the world! It can easily be a mile from your room to the conference center. (Plus… dance parties! I’ll be participating in the Anchor Dance-Off in Booth #170.)

Pack an extra collapsible duffle bag for swag if you’re into it – but remember… you can also say “no thank you”. It’s easy to get lost in the freebie frenzy, but do you really need another stress ball? That said, some of the stuff will be too good to pass up and you want to make sure you have room to carry it home.

The breakout rooms are often FREEZING! Bring a wrap, poncho or sweatshirt.

However, it’s also Orlando in June and there’s a pool, as well as a full waterpark with a lazy river and waterslides, included at no extra charge as part of the Scaling New Heights room cost. Pack your swimsuit!

Bring a refillable water bottle (or reuse a plastic bottle) and/or coffee/tea mug; there will be dispensers, and also, the water in your hotel room is fine to drink.

Bring battery packs and chargers – often the rooms are in a basement and your cell struggles and chews up your battery; plus you’ll want to be on the conference app, your association’s Slack, and you’ll probably text a lot.

Conference hotels are pricey! Buy food & drink at a nearby convenience store if you’re going to want snacks or a bottle or box of wine outside of the usual meals and parties. Keep in mind that the Marriott is a Pepsi products hotel, so if you need your Coke, best buy some as well. The closest 7/11 is a mile away, so hit it up first-thing on the way from the airport so you get it all in one visit, or get a group of folks together to split the cost of a 6-seater Lyft XL. (While you’re there, pick up some epsom salts to soak your feet.)

Ordering grocery or restaurant food delivery is often a lot cheaper than eating at the hotel restaurants. I’ve heard great things about Vacation Grocery Delivery in Orlando.

Speaking of the hotel restaurants, the reservations book up very quickly. If you know you’ll want to eat out on a given night, go ahead and reserve as soon as you can.

There are coffeemakers in the rooms, but only the kind that take those disposable pod-cup things. There is a Starbucks and a market but sometimes the lines are long. You may want to bring a portable tea kettle or coffeemaker; this is ours.

Carry small bills for tipping bartenders at the various happy hours, socials, parties and receptions. They work hard and many attendees don’t think to bring cash.

Bring earplugs for sleeping and loud parties.

All that said, don’t overpack. We’re only there for four days and you can re-wear some of your clothing. You don’t want to get stuck spending most of your final night re-packing your whole wardrobe. You’ll probably need less stuff than you think.

There’s usually a spot where you can store your luggage on the last day, after checking out (rather than with the hotel concierge).

Dress code: BE YOURSELF. Many people are in sweats and jeans, others are in power-suits or dresses, and some of us love dressing up in-costume and wearing tiaras whenever we get the chance. Wear what makes you feel most like yourself.

Tip Four — TRAVEL CONSIDERATIONS

Mears Transportation offers shuttle service from Orlando International Airport to the hotel for $16 per person, each way. Reserve in advance here. Given that taxi fare is about $55, the shuttle is usually the better way to go, especially with luggage.

Included in the cost of rooms in the Scaling New Heights room block is daily scheduled shuttle service to all four Disney Parks & Disney Springs.

Plan for ample travel time while in Orlando, whether you’re on foot or in a vehicle. The location is “just outside the entrance to Disney World” but each property is so massive that it often takes half-an-hour to get anywhere.

Once you’ve met a bunch of folks at the conference, consider coordinating to share a cab back to the airport when you depart, if the shuttle service timing doesn’t work for you and you don’t have too much luggage.

Check in early and skip the SNH check-in lines. On Sat, June 15 from 12 PM-6 PM and again on Sunday starting at 8 AM, you can head to the Registration Desk near the Cypress Ballroom. Remember to bring your ID.

Tip Five — NETWORKING

Represent your tribe… for example, last year at QB Connect, the Bookkeeping Buds all wore tiaras for one of the sessions where a member was presenting. I also always bring my favorite Bookkeeping Buds bag and use it instead of the conference one (it not only is a nice talking point, but it also is easier to find if you leave it behind somewhere). Many folks love wearing t-shirts from their favorite apps – Kim Noh even has her own tee that has logos of her tech stack!

Stay connected via Slack, social media, and texts throughout the conference. Often folks in your group will save a block of seats at the mainstage presentations, or will give a heads-up when a particular session is fabulous or misses the mark.

Bring business cards – digital, paper, or a paper one with a QR code (or QR code stickers). I started using HiHello late last year and I printed out a QR code and taped it to my phone case, which makes it easy for folks to scan, but also a great way for someone to find me if I lose my phone. These days the vendors usually just scan your badge to get your info, but they do sometimes have raffles where you can drop an old-school card in an old-school fishbowl; I have a different set of b-cards I use for these with an email that routes to a different folder.

Prepare your elevator pitch – who are you, what do you do, why are you here, what makes you different? What will I want to remember about meeting you?

Tip Six — TAKE CARE OF YOURSELF

Sleep well the week leading up to the conference – the sessions start early, the parties go late, and there’s always something happening in the hotel bar.

Put your badge on the inside of the doorknob when you get back to your room, so that you remember to grab it on your way out. They are strict about not letting anyone in without it.

It’s okay to skip the morning session if you were up late, or to take a nap during a mainstage or between events. Give yourself some grace.

But be careful about how late you stay up and how much you drink. You don’t want to miss something valuable or feel sick just because you lost track of yourself. There’s a cool “bracelet trick” I learned years ago… put as many bracelets on your left wrist as drinks you’ll allow yourself. Move one bracelet to the right wrist with each drink. Once your left wrist is empty, you cut yourself off. Another trick is to re-use the same glass each time you get another adult beverage — filling it up with water between drinks… you have to finish the water before allowing yourself a refill. And this may go without saying, but make sure to eat a full meal to soak up the bevvies.

Consider arriving a day early or leaving a day late so you can see the sights or enjoy the hotel amenities. I find that every place I go has something to offer.

Tip Seven — SET YOURSELF UP FOR SUCCESS

There is a “New Attendee Orientation” on Sunday, June 16 at 9 AM in the Crystal Ballroom, Room J. Usually they will place veteran conference-goers at each table to help guide rookies and answer questions. There is a “Practice Advancement Breakfast” afterwards in the Palms Ballroom Sabal Room. It requires an RSVP in the app, but is free of charge.

There are always seats up-front, even when a session looks full. Don’t be nervous about walking right up there, even if it’s a few minutes into the session. No one’s looking at you, and no one cares.

That said, feel free to ditch a class if it’s not what you were hoping for or expected. There are other workshops that will be better worth your valuable time – or maybe it’s an opportunity to visit with vendors or network with colleagues.

Take a photo of the Exhibit Hall map so you can easily zoom in/out and orient the phone so you’re pointing the right direction.

Take lots of notes – notebook, e-ink pad, tablet, laptop… however works best for you. (In fact, as a paper-note-taker, I plan to check out my friends’ Remarkables and Supernotes as one of my research goals for the conference.)

In that notebook, keep one page aside for notes that are about client-specific problems that you will solve when you get back home; and another for non-client-specific items you will address. Try to restrict that second list to only 2-3 things – it’s impossible to implement every shiny new idea you come across. Those will hang around in your head and you’ll get a chance to learn more at the next conference, by which point maybe you’ll have a new set of goals.

Don’t miss Nicole Davis‘ keynote on Wednesday, June 19th (aka Juneteenth) at 9 am! She is a beautiful human being and I cannot wait to find out what she has to share with us.

It’s natural to be nervous, but you can do this! Even extroverts struggle with meeting new people sometimes. Move through that shyness or fear and lean into the fact that almost everyone here came alone; everyone had a first conference where they didn’t know anyone; and everyone is here to meet other people and develop their practices. We have so much in common… sit at a lunch-table where you don’t know anyone and introduce yourself. Ask why they’re here and what they’re enjoying most. Find out where they’re from and what their specialty is. Tell them your goals and ask if they have advice. Ask them what their tech stack is and share your struggles with your choices and vendors and all the things. We will never run out of topics to talk about with each other, because there is so much to learn in our industry. Plus, chances are that these are folks who are as passionate about what they do as you are, or they wouldn’t be here in the first place.

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.

Recently, I had the pleasure of joining Adam Lean of The CFO Project on his podcast, “Escaping the Accountant’s Trap,” to discuss imposter syndrome — what it really means, how to know if you have it (or are simply learning something new), and practical tips for overcoming those feelings of being a fraud.

The inspiration for the episode came when I heard Adam speak on Veronica Wasek’s 5-Minute Bookkeeper Facebook group (a must-follow if you’re a bookkeeper, in my opinion). He has so much valuable knowledge to share, but I felt like the delivery was oriented toward tax professionals and other accountants, rather than her main audience. In my experience, bookkeepers looking to offer CFO advisory services are in a very different position than accountants moving into a new realm, especially marginalized groups like women and minorities, and so I reached out to suggest we work together to talk about the topic of imposter syndrome — and what we can do to push past sentiments of self-doubt, when in fact what we’re doing is building on our existing foundations of knowledge and exploring new perspectives.

Studies show that 70% of people experience “imposter syndrome” at some point… defined as a fear that you’re inadequate or incompetent — despite evidence to the contrary. Dr. Valerie Young has a great book on why capable people experience it. From my research with psychologists and therapists, I’ve learned that medically, something only becomes a “syndrome” if it’s seriously impeding your life, paralyzing you so that you can’t do things you would otherwise excel at or enjoy — so my first goal in spreading the word on this topic is: please don’t feel like there’s something wrong with you if you’re feeling self-doubt. This isn’t a “syndrome”… in fact, this is natural, especially for women — this is an understandable, genuine reaction to being condescended to our whole lives.

As for being able to tell the difference, think of it this way: Any new task by definition puts you in a position where you don’t know how to do your job. Having more background makes it so the percentage of your job you don’t know how to do is smaller. But climbing that learning curve is always part of the experience — and that is what makes us feel exposed or fraudulent. Education, testing, and experience are the three best solutions to this – they help you learn what you need to know, and they also build confidence.

This was not a paid partnership — I gave my time freely to record and promote this episode because it’s simply an important topic to me, and I want to give it more space in the airwaves so that bookkeepers know they’re not alone in their doubt, and yet they are uniquely positioned to branch into advisory services.

We covered a lot of ground in this episode — here’s a breakdown: 0:00–4:00 Introductions 5:37 What is imposter syndrome? How do I know if I have imposter syndrome? 11:52 Why bookkeepers are uniquely positioned to advise business owners doing CFO services! 16:42 CPA asks “I’m afraid that my lack of real-world business experience will hold me back. What are your thoughts?”

I hope you get something helpful from our conversation! It’s essential that we share our questions, doubts, struggles and challenges in order to discover that we’re not alone, and to provide support for our colleagues, ultimately affecting the mental health of the whole industry, and assisting small businesses in their important community-building work. (Another passion project of mine — come see me present the panel “Vulnerability as a Strength” at Bridging the Gap this July!)

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.

Tax season is over. Take a deep breath – whether you’re a bookkeeper or tax preparer, you’ve endured plenty of stress these past months, and now you’re in the perfect space between vacation and conference season to look back and figure out how to make it go better next year.

That’s what we do in our firm, anyway; I learned an amazing lesson from one of my favorite instructors, Tom Gorczynski, to plan for next tax season while the pain is still fresh in your mind! We schedule a company-wide zoom meeting, and everyone fills out a survey beforehand that asks about what worked, what didn’t, what they’d like to see go differently, who their favorite and least-favorite clients are, and why. This helps us incrementally improve year-over-year, and makes sure everyone has a voice. Then we send out cocktail kits and snacks to everyone, we celebrate, and we brainstorm. We even vote clients “off the island” together.

One of the themes that comes up every year is the need to move more clients off QuickBooks Desktop and onto QuickBooks Online. I know, groan… yet another talking head telling you to make the shift! At this point you’ve been bombarded with information on all the benefits of moving to QBO, so I won’t bore you with those. I’ll just share my own experience.

It was becoming more and more of a drag to coordinate with Desktop clients to review their books, and the new subscription structure made it confusing and frustrating to know who was on which version and how to make the most of what they were paying for. And of course, there were constant client fears around Intuit’s messaging, worrying they were going to stop supporting their product. But the biggest stressor for us was that it was actually getting hard to find junior bookkeepers who had ever worked with the Desktop program. (No joke. How about that for making a certain dancing accountant feel old?)

I assure you, I absolutely *hated* QBO for years; it was a clunky beast that didn’t have some of the most basic functionality that Desktop did – and I’m not just talking about the early days; this went on far too long and alienated many users. And while I held out for ages in moving to QBO, especially for certain types of clients that really benefited from what QBDT had to offer, I finally realized that it’s gotten to the point where the features I love about the Online version far outweigh its negatives. Between the concerted effort that Ted Callahan, Jessica McCracken and their team have made to actually listen to our community and implement some of the most-loved features; the fact that most third-party apps and tools no longer work with Desktop; and the advent of RightTool, an amazing browser extension by industry superstar Hector Garcia that supercharges what QBO has to offer… it’s time. It’s really time. QBO is now light-years ahead of almost anything that QBDT can do.

The point of outlining all this isn’t to convince you that you should migrate your remaining Desktop clients to QBO. It’s to suggest that when you do – follow my lead, and use exactly these reasons in your messaging. This became our mantra for communicating the value of converting, and it worked; at this point we only have one client left who needs to make the shift.

Think about it: your clients and your team members trust you, more than anyone else, to make smart and thoughtful decisions with everyone’s well-being in mind. If you convey the messaging that QBO is listening to us and responding to our requests, that RightTool will make you more efficient, and third-party apps will serve your clients’ needs better than the previous solutions, they will believe you, you’ll get buy-in, and in our experience, we found that clients were overwhelmingly positive and enthusiastic (though understandably still nervous) about the change.

Once you’ve got buy-in, it’s a simple matter of following some practical tips and advice to make sure the execution is done well.

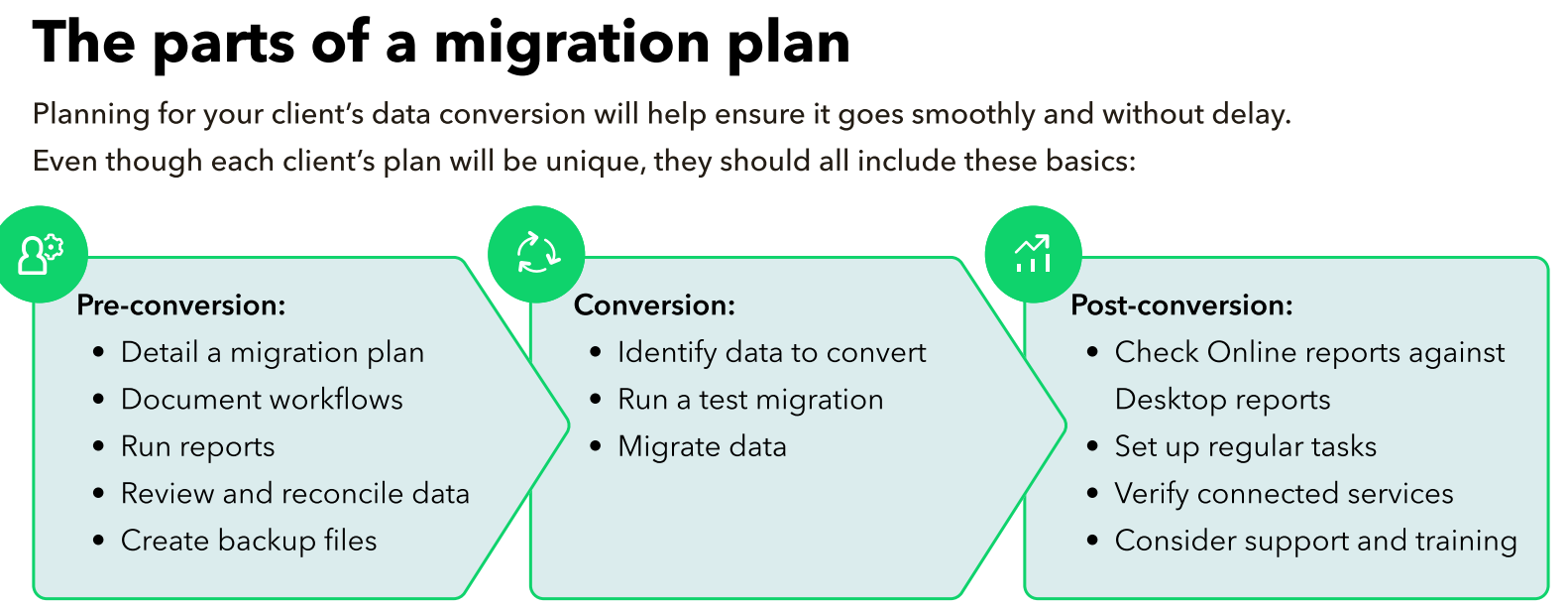

Understand the Conversion Process Intuit came out with a free conversion tool a few years ago that they keep tweaking to make it better; the most recent improvements announced at last year’s QB Connect blew me away – you can now batch migrate clients, meaning “do a ton at once and be done with it”. To be honest, it kind of made me wish I had waited to convert some of ours! However, as straightforward as they make it to migrate data from QBD to QBO, you do have to ensure your QBDT file is ready for the transition. This means backing up, running a verification on the file, ensuring it’s under the maximum target limit, and cleaning up any weirdo issues that have been hiding or buried for years, especially if you don’t regularly do a verification and rebuild. And most importantly, reviewing your “all dates” financial statements beforehand, exporting them, and comparing the same reports afterwards is essential.

Technical Resources for Conversion

I mentioned Intuit’s Conversion Tool, which guides you through the process step-by-step; they also have a QuickBooks Conversion Toolkit with checklists, webinar links, guides, client materials, and even a link to book a call to have Intuit do the conversion for you – just head here and then click on the “How to migrate” button to download the toolkit or set up a call. If you prefer your info from a third-party source, Hector Garcia does a short walkthrough on his YouTube channel, and Alicia Katz-Pollock is offering an Earmark webinar on May 21st. And if you have any concerns whatsoever about the process, consider outsourcing the job. We worked with CMB Hero and had a good experience, and I know DL & Associates does migrations as well; there are probably hundreds of companies or even trusted colleagues who’ve gone through the process before and can help you make sure it goes smoothly.

Research Third-Party Apps Before Converting

There are some super-fabulous apps out there that we love to use for syncing daily Point of Sale data, such as Synder, Bookkeep, and Shogo. But you need to look at the client’s needs and determine how they’ll be met in the new QBO world before making the shift – not all sync programs work with all POS platforms. Do demos, consult with colleagues, and figure out the timeline for implementing – in other words, not only the migration of QBDT data to QBO, but setting up the new system to work with the POS and get it all running. Our experience has been that some up-front planning saves loads of effort on the far end (which is when you’re pressed for time so the client can get back up-and-running).

Prepare Desktop Clients For The Change

And sticking with the theme of up-front planning… a little client hand-holding goes a long way. What they’re looking for is to follow your lead as their trusted advisor. The more you can compare and contrast their existing workflows and procedures with the new system, the more comfortable they’ll be with your proposal to move to QBO. Ideally, you already have Standard Operating Procedures in place for each of your clients. I wince as I type this, because I get that this is the “ideal” and not necessarily your reality – in all honesty, we’re still in the process of making sure each client has clear and detailed SOPs for every scenario. But this is a golden opportunity. Your instructions – in Word, an Excel checklist, Loom videos, or a project management app like Keeper, Financial Cents, or Asana – will build trust, making it much easier for you to illustrate to the client that this is a manageable change and that you’ve anticipated their needs. Side bonus: way less stress when a client (or your firm) loses a trusted team member and a new one needs to be trained ASAP.

To illustrate: in going through all the steps that a client’s office manager would complete each month as part of her billing process, and reproducing/ rewriting them using QBO, I noticed that she would no longer be able to run a particular report – at this point I had to decide whether we would come up with a different way for her to perform the same task, or whether we would track the data with a different feature in QBO so that she could run the report she was used to. Both approaches were fair; but the point is that I wouldn’t have noticed this change without walking through the process of retooling the procedures. This built trust with the client and made them more open-minded about making the change, because they knew we were actively anticipating and removing any stumbling blocks.

Client & Staff Training and Familiarization

As you know, transitioning to QBO doesn’t just involve moving data; it’s also about adapting to a new user environment. You’ll want to invest time in training sessions provided by Intuit or certified trainers like Royalwise (my personal favorite – I’ve been studying from Alicia for as long as I can remember). Intuit also offers an ongoing monthly session called QBO In The Know, which I encourage all my team members to attend as part of their paid training hours – this ensures that you don’t just get up-to-date, but that you stay that way, as the QBO ecosystem is constantly improving and new features are released every month. Hector Garcia’s YouTube channel is an endless wealth of information (I once hired a senior accountant with no degree and no certification based on the fact that she learned QBO by watching every single one of his videos. She’s now our Senior Accountant). Lastly, remember that QBO has a demo company! It’s a sandbox – have at it, and let your team practice without the risk of affecting real data.

Start by getting your client and team members’ buy-in. Take advantage of the available resources, and invest in training. With communication and planning, both your firm’s and your clients’ bookkeeping experience will end up better than it was with Desktop – we don’t have a single client that regrets having migrated, despite the fact that we all miss this-or-that feature (everyone’s got their favorite). But I promise it will be replaced by a new favorite. Remember, the goal is not just to convert data, but to enhance the overall efficiency and effectiveness of your accounting practices and those of your clients.

So… take that deep breath, plan for the future, and enjoy the heck out of that moment next tax season when you hear someone go, “oh wow, this really is so much better than it used to be!”

Note! As my readers know, I am downright fanatical about transparency and full disclosure (often to my detriment, as you may have noticed that I have a wildly popular award-winning blog that is non-monetized). Though this particular post is a paid partnership with Intuit, I want you to know that a) I wanted to write an article on QBDT–>QBO conversions anyway, but couldn’t find the time; getting paid allowed me the break from client work I needed to make it happen; and b) they didn’t delete a single thing when I presented it. In fact, they were totally cool with all my Intuit-bashing… which made me pretty impressed with them, to be honest. That’s twice now — let’s see if they go for a three-fer!

QuickBooks ProAdvisors are first nominated, and then go through a lengthy vetting process, before eventually opening up to a public vote. Applicants for this prestigious award are ranked based on their performance across various categories, measuring everything from QuickBooks knowledge and continuing education, to utilizing the best tools and partner apps within the QuickBooks ecosystem. Real-world experience with clients is a requirement. Winners have said the Top 100 recognition by peers and their industry has opened doors and provided inspiration and new perspectives, and I agree; I have no way of knowing for sure, but I imagine this recognition made a difference when I was selected to speak at Scaling New Heights for my first time.

I would love to express sincere appreciation to Gary DeHart, Murph, and the entire Insightful Accountant team for their hard work evaluating the nominees — it’s quite special to receive an award from a publication that has been a trusted go-to resource for so long: especially this year, having been invited to be a member of their inaugural advisory board.

Special thanks to all those who voted, in particular my esteemed colleagues and valued clients. It’s extremely exciting to share space with luminaries in the Intuit QuickBooks world such as Lynda Artesani, Carla Caldwell, Sharrin Fuller, Matthew Fulton, Caleb Jenkins, Alicia Katz Pollock, Michelle Long, Kim Noh, and Veronica Wasek.

But this year is even more special than the last, for another important reason. If you’re a regular reader, you know how enthusiastic I am about one of my professional organizations in particular: Bookkeeping Buds. Well, this year, every single one of the amazing women in this group that was nominated for the Top 100 received a place in either the main tier or the “Top 25 Up-n-Coming” award. This really says something about the community that Cindy Schroeder has built. We support each other — and something that I see in common with all our Top 100 and 25 Up-n-Comers is that every one of them focuses on helping others. I feel like that’s a huge part of what Buds is about and it feels great to be recognized for it! As Cindy often points out, we are truly stronger together… though technically in competition, we realize that when we support each other unabashedly, the rising tide we create lifts all boats. Special shout-outs to this group: Melissa Miller Furgeson, Kelsey Elliott, Wendy Kelley, Deb Kilsheimer, Questian Telka, and Hope Brown. You continuously inspire me to rise to your example of sisterhood.

Looking forward to the formal announcement at Scaling New Heights. If you see me there, please come on up and introduce yourself!

From the 2023 Insightful Accountant Top 100 Awards Ceremony.

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.