Thanks yet again, and as always, to Lisa Simpson from the AICPA Town Hall for her regular updates on what’s going on with Employee Retention Credit processing at the IRS. I can trust this team to make sure I’m getting the latest information, free from rumors and gossip, and that I’m able to both quell my clients’ concerns and also manage their expectations.

I had just been hearing some rumblings in one of my professional associations — someone had said, “seems inevitable that anyone who filed an ERC claim after September 2023 will need to file a lawsuit to get the claim paid,” and went on to suggest that it would be a great opportunity for a law firm, and wanted to know if we had referrals in this space.

First off, it made me nervous — our remaining ERC claims, all for deserving small business and non-profit clients of a colleague, worked really hard to make sure we had what we needed to submit their claims by January 31st, 2024, since there was pending legislation that might retroactively end the program after that date. They all were informed that it might be a year or more before they received the money, given the IRS moratorium — but certainly none of us expected to line the pockets of an attorney in order to get the claims paid out. And in fact, the claims were mostly small enough that my guess is most lawyers wouldn’t bother with them.

Secondly… it made me suspicious. On what basis was this guy saying a lawsuit would be “inevitable”? I attend every single AICPA Town Hall and hadn’t heard anyone suggest this. And what a sad thing to suggest it would be a “great opportunity” for a law firm — to specialize in making money off those desperate to finally receive what they and their accountants had already worked so hard to obtain.

As usual, I decided to quell those fears until the next AICPA Town Hall, and I’m so glad I did, as Lisa Simpson made ERC the first topic in her Technical Update. She explained the recent IRS news release that likely triggered the unfounded rumblings I was hearing, as well as referenced a new Journal of Accountancy article that delved deeper.

My takeaway was that: while 10-20% of claims are clearly fraudulent, and the IRS is in the process of denying them; and another 60-70% show an unacceptable level of risk and will be examined carefully — there are also between 10% and 20% of the claims show a low risk. The IRS “will begin judiciously processing” more of these claims, and, according to the release, expects some of these payments to be made later this summer.

To me, that’s all good news. It means they’re working through the piles and expediting the ones that have straightforward claims where the businesses played by the rules, processing the oldest ones first. The rest will be examined more critically, or in the case of blatant fraud, flat-out denied.

The one disappointing piece of information is that no claims submitted during the moratorium will be processed at this time. But at least we know the backlog is being cleared to make way for them. Since the moratorium was put in place, the IRS has received over 17,000 claims per week.

I’ve let my clients know that they shouldn’t budget for these dollars for at least another year, but that there’s no reason to presume they won’t eventually receive the claims that are due to them.

And yet again I learned that if something sounds sensational and suspicious… it might not be grounded in evidence and analysis. Rely only on your trusted advisors for the education and resources that will help you guide your small business clients. (And then provide links to those resources to the sensationalists who spread misinformation.)

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.

One of my favorite books when I was a kid was “Hail, Hail, Camp Timberwood,” about a girl who goes to summer camp for her first time. She’s standing around, feeling (and probably looking) uncomfortable as all the return campers are running around, hugging each other, excited to be reunited. All of a sudden, someone runs up to her and gives her a big hug and says how happy she is to see her again. After a moment of total confusion, the girl leans in and says, “Don’t worry – we don’t actually know each other. I was just feeling left out and figured I’d join ‘em.” The two of them become fast friends and go off hugging others who looked out of place and letting them in on the joke. Before you know it, the entire place was full of everyone running around hugging each other and laughing.

While I can’t say this is likely to happen exactly like that at the upcoming Scaling New Heights conference in Orlando, I also wouldn’t be that surprised if it did. There will be heaps of people reuniting for the first time since last year (check out my video blog about those amazing takeaways as well as my recent article for Insightful Accountant). But there will also be loads of first-timers attending, who are nervous and out of their element. Find the other wallflowers and go up to them – tell them it seemed like maybe they didn’t know anyone there, either, and do they want to eat lunch together or go to a vendor booth or grab a drink? You’ll be delighted and surprised at how many of these folks you’ll stay in touch with through the years. Remember, progressive accountants and bookkeepers such as the kind you’ll find at SNH – especially those who go year after year – are excited you’re there, and they want to help make your experience better. Introduce yourself to someone who looks like they “belong” and say that you’re new, and not sure where to begin. I am sure they’ll point you in the right direction, take you under their wing, or introduce you to someone who might be a great conference buddy.

For today’s blog post, I’m going to be that conference buddy, and share with you my Expert Tips for Attending Scaling New Heights 2024.

And Joe Woodard himself hosted one on Maximizing Your Experience at Scaling New Heights 2024 — catch the recording here, and they’ve kindly made the slides available for all attendees. Lots of great info on ’em — definitely worth the download.

Plan ahead, make a schedule, but be comfortable diverging from it; that way you don’t waste time figuring out what to do in the moment, but you also don’t miss the organic opportunities that arise.

Make a list of vendors you’d like to meet; they’re often very busy during open Exhibit Hall time; it might be helpful to set up a time with them to meet during a session when the Hall is less busy. Bring a list of questions you’d like to have answered. Narrow your scope… it’s impossible to visit everyone. Pick a few areas of interest, look into which vendors serve those areas, and focus on them.

Connect on social media with others who will be attending, whether it’s in a Facebook group like Woodard Group of the Americas or QB Community Live, LinkedIn, or other platform, you can always use #SNH24 to find out who you already know that might be going. Engage and make plans ahead of time.

Check with your sales reps and vendors for the tools you love best — whether you’re already using them or plan to implement this year — to see if they are hosting any customer dinners or get-togethers. Same with professional associations you might be considering joining, like Bookkeeping Buds, Realize, or Roundtable.

Tip Two — DOWNLOAD AND USE THE MOBILE APP

The training schedule on the Woodard website does a nice job of giving you a visual to see which sessions are held concurrently, and which are 50-minutes versus 100 or 120-minutes. It also lists the course objectives for each session, below the description, which the app does not. However, you can only register for a session using the app or the mobile app — not via the main website’s training schedule. (The Scaling New Heights website agenda/ training schedule and the SNH app do not sync with each other.)

If you still have the app on your phone from last year, it will work! You just have to click “JOIN” on the new conference. Otherwise, check out the slides below from Woodard for app instructions, as well as my friend Mariette Martinez’s how-to video for the mobile app.

It’s definitely helpful to the community if you register ahead-of-time for the classes that interest you (such as “The Tax-Ready Bookkeeper”, my session at 12 noon on Sunday, June 16th)! This is how they determine which rooms will be assigned for each one. If there’s a lot of interest in a particular topic, they’ll give it a bigger room, and that makes life easier for everyone.

You can’t “like” or “favorite” any of the other sessions at the same time, as is the case with some apps… you can only “register”, and only for one per time slot. However, you can export as many sessions as you like from either the app or web version of the app to your calendar, which could be a workaround if you’re interested in more than one and want to track them all.

The app won’t let you register if it’s full. But that doesn’t mean you shouldn’t try to attend anyway! Lines will form for the “sold-out” sessions, and they will let additional people in if there’s capacity, which there usually is – get there early to be near the front of the line. There is almost always extra room and I’ve rarely been turned away.

If you click on the session, it will show you the description, as well as speaker info. If you click on the speaker, it will show their bio and all the sessions they’re teaching at the conference, as well as a link to their website. This is a great way to research which instructors you’d like to hear.

Tip Three — PACK WISELY AND COMFORTABLY

Wear comfortable shoes – this is the largest Marriott in the world! It can easily be a mile from your room to the conference center. (Plus… dance parties! I’ll be participating in the Anchor Dance-Off in Booth #170.)

Pack an extra collapsible duffle bag for swag if you’re into it – but remember… you can also say “no thank you”. It’s easy to get lost in the freebie frenzy, but do you really need another stress ball? That said, some of the stuff will be too good to pass up and you want to make sure you have room to carry it home.

The breakout rooms are often FREEZING! Bring a wrap, poncho or sweatshirt.

However, it’s also Orlando in June and there’s a pool, as well as a full waterpark with a lazy river and waterslides, included at no extra charge as part of the Scaling New Heights room cost. Pack your swimsuit!

Bring a refillable water bottle (or reuse a plastic bottle) and/or coffee/tea mug; there will be dispensers, and also, the water in your hotel room is fine to drink.

Bring battery packs and chargers – often the rooms are in a basement and your cell struggles and chews up your battery; plus you’ll want to be on the conference app, your association’s Slack, and you’ll probably text a lot.

Conference hotels are pricey! Buy food & drink at a nearby convenience store if you’re going to want snacks or a bottle or box of wine outside of the usual meals and parties. Keep in mind that the Marriott is a Pepsi products hotel, so if you need your Coke, best buy some as well. The closest 7/11 is a mile away, so hit it up first-thing on the way from the airport so you get it all in one visit, or get a group of folks together to split the cost of a 6-seater Lyft XL. (While you’re there, pick up some epsom salts to soak your feet.)

Ordering grocery or restaurant food delivery is often a lot cheaper than eating at the hotel restaurants. I’ve heard great things about Vacation Grocery Delivery in Orlando.

Speaking of the hotel restaurants, the reservations book up very quickly. If you know you’ll want to eat out on a given night, go ahead and reserve as soon as you can.

There are coffeemakers in the rooms, but only the kind that take those disposable pod-cup things. There is a Starbucks and a market but sometimes the lines are long. You may want to bring a portable tea kettle or coffeemaker; this is ours.

Carry small bills for tipping bartenders at the various happy hours, socials, parties and receptions. They work hard and many attendees don’t think to bring cash.

Bring earplugs for sleeping and loud parties.

All that said, don’t overpack. We’re only there for four days and you can re-wear some of your clothing. You don’t want to get stuck spending most of your final night re-packing your whole wardrobe. You’ll probably need less stuff than you think.

There’s usually a spot where you can store your luggage on the last day, after checking out (rather than with the hotel concierge).

Dress code: BE YOURSELF. Many people are in sweats and jeans, others are in power-suits or dresses, and some of us love dressing up in-costume and wearing tiaras whenever we get the chance. Wear what makes you feel most like yourself.

Tip Four — TRAVEL CONSIDERATIONS

Mears Transportation offers shuttle service from Orlando International Airport to the hotel for $16 per person, each way. Reserve in advance here. Given that taxi fare is about $55, the shuttle is usually the better way to go, especially with luggage.

Included in the cost of rooms in the Scaling New Heights room block is daily scheduled shuttle service to all four Disney Parks & Disney Springs.

Plan for ample travel time while in Orlando, whether you’re on foot or in a vehicle. The location is “just outside the entrance to Disney World” but each property is so massive that it often takes half-an-hour to get anywhere.

Once you’ve met a bunch of folks at the conference, consider coordinating to share a cab back to the airport when you depart, if the shuttle service timing doesn’t work for you and you don’t have too much luggage.

Check in early and skip the SNH check-in lines. On Sat, June 15 from 12 PM-6 PM and again on Sunday starting at 8 AM, you can head to the Registration Desk near the Cypress Ballroom. Remember to bring your ID.

Tip Five — NETWORKING

Represent your tribe… for example, last year at QB Connect, the Bookkeeping Buds all wore tiaras for one of the sessions where a member was presenting. I also always bring my favorite Bookkeeping Buds bag and use it instead of the conference one (it not only is a nice talking point, but it also is easier to find if you leave it behind somewhere). Many folks love wearing t-shirts from their favorite apps – Kim Noh even has her own tee that has logos of her tech stack!

Stay connected via Slack, social media, and texts throughout the conference. Often folks in your group will save a block of seats at the mainstage presentations, or will give a heads-up when a particular session is fabulous or misses the mark.

Bring business cards – digital, paper, or a paper one with a QR code (or QR code stickers). I started using HiHello late last year and I printed out a QR code and taped it to my phone case, which makes it easy for folks to scan, but also a great way for someone to find me if I lose my phone. These days the vendors usually just scan your badge to get your info, but they do sometimes have raffles where you can drop an old-school card in an old-school fishbowl; I have a different set of b-cards I use for these with an email that routes to a different folder.

Prepare your elevator pitch – who are you, what do you do, why are you here, what makes you different? What will I want to remember about meeting you?

Tip Six — TAKE CARE OF YOURSELF

Sleep well the week leading up to the conference – the sessions start early, the parties go late, and there’s always something happening in the hotel bar.

Put your badge on the inside of the doorknob when you get back to your room, so that you remember to grab it on your way out. They are strict about not letting anyone in without it.

It’s okay to skip the morning session if you were up late, or to take a nap during a mainstage or between events. Give yourself some grace.

But be careful about how late you stay up and how much you drink. You don’t want to miss something valuable or feel sick just because you lost track of yourself. There’s a cool “bracelet trick” I learned years ago… put as many bracelets on your left wrist as drinks you’ll allow yourself. Move one bracelet to the right wrist with each drink. Once your left wrist is empty, you cut yourself off. Another trick is to re-use the same glass each time you get another adult beverage — filling it up with water between drinks… you have to finish the water before allowing yourself a refill. And this may go without saying, but make sure to eat a full meal to soak up the bevvies.

Consider arriving a day early or leaving a day late so you can see the sights or enjoy the hotel amenities. I find that every place I go has something to offer.

Tip Seven — SET YOURSELF UP FOR SUCCESS

There is a “New Attendee Orientation” on Sunday, June 16 at 9 AM in the Crystal Ballroom, Room J. Usually they will place veteran conference-goers at each table to help guide rookies and answer questions. There is a “Practice Advancement Breakfast” afterwards in the Palms Ballroom Sabal Room. It requires an RSVP in the app, but is free of charge.

There are always seats up-front, even when a session looks full. Don’t be nervous about walking right up there, even if it’s a few minutes into the session. No one’s looking at you, and no one cares.

That said, feel free to ditch a class if it’s not what you were hoping for or expected. There are other workshops that will be better worth your valuable time – or maybe it’s an opportunity to visit with vendors or network with colleagues.

Take a photo of the Exhibit Hall map so you can easily zoom in/out and orient the phone so you’re pointing the right direction.

Take lots of notes – notebook, e-ink pad, tablet, laptop… however works best for you. (In fact, as a paper-note-taker, I plan to check out my friends’ Remarkables and Supernotes as one of my research goals for the conference.)

In that notebook, keep one page aside for notes that are about client-specific problems that you will solve when you get back home; and another for non-client-specific items you will address. Try to restrict that second list to only 2-3 things – it’s impossible to implement every shiny new idea you come across. Those will hang around in your head and you’ll get a chance to learn more at the next conference, by which point maybe you’ll have a new set of goals.

Don’t miss Nicole Davis‘ keynote on Wednesday, June 19th (aka Juneteenth) at 9 am! She is a beautiful human being and I cannot wait to find out what she has to share with us.

It’s natural to be nervous, but you can do this! Even extroverts struggle with meeting new people sometimes. Move through that shyness or fear and lean into the fact that almost everyone here came alone; everyone had a first conference where they didn’t know anyone; and everyone is here to meet other people and develop their practices. We have so much in common… sit at a lunch-table where you don’t know anyone and introduce yourself. Ask why they’re here and what they’re enjoying most. Find out where they’re from and what their specialty is. Tell them your goals and ask if they have advice. Ask them what their tech stack is and share your struggles with your choices and vendors and all the things. We will never run out of topics to talk about with each other, because there is so much to learn in our industry. Plus, chances are that these are folks who are as passionate about what they do as you are, or they wouldn’t be here in the first place.

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.

Recently, I had the pleasure of joining Adam Lean of The CFO Project on his podcast, “Escaping the Accountant’s Trap,” to discuss imposter syndrome — what it really means, how to know if you have it (or are simply learning something new), and practical tips for overcoming those feelings of being a fraud.

The inspiration for the episode came when I heard Adam speak on Veronica Wasek’s 5-Minute Bookkeeper Facebook group (a must-follow if you’re a bookkeeper, in my opinion). He has so much valuable knowledge to share, but I felt like the delivery was oriented toward tax professionals and other accountants, rather than her main audience. In my experience, bookkeepers looking to offer CFO advisory services are in a very different position than accountants moving into a new realm, especially marginalized groups like women and minorities, and so I reached out to suggest we work together to talk about the topic of imposter syndrome — and what we can do to push past sentiments of self-doubt, when in fact what we’re doing is building on our existing foundations of knowledge and exploring new perspectives.

Studies show that 70% of people experience “imposter syndrome” at some point… defined as a fear that you’re inadequate or incompetent — despite evidence to the contrary. Dr. Valerie Young has a great book on why capable people experience it. From my research with psychologists and therapists, I’ve learned that medically, something only becomes a “syndrome” if it’s seriously impeding your life, paralyzing you so that you can’t do things you would otherwise excel at or enjoy — so my first goal in spreading the word on this topic is: please don’t feel like there’s something wrong with you if you’re feeling self-doubt. This isn’t a “syndrome”… in fact, this is natural, especially for women — this is an understandable, genuine reaction to being condescended to our whole lives.

As for being able to tell the difference, think of it this way: Any new task by definition puts you in a position where you don’t know how to do your job. Having more background makes it so the percentage of your job you don’t know how to do is smaller. But climbing that learning curve is always part of the experience — and that is what makes us feel exposed or fraudulent. Education, testing, and experience are the three best solutions to this – they help you learn what you need to know, and they also build confidence.

This was not a paid partnership — I gave my time freely to record and promote this episode because it’s simply an important topic to me, and I want to give it more space in the airwaves so that bookkeepers know they’re not alone in their doubt, and yet they are uniquely positioned to branch into advisory services.

We covered a lot of ground in this episode — here’s a breakdown: 0:00–4:00 Introductions 5:37 What is imposter syndrome? How do I know if I have imposter syndrome? 11:52 Why bookkeepers are uniquely positioned to advise business owners doing CFO services! 16:42 CPA asks “I’m afraid that my lack of real-world business experience will hold me back. What are your thoughts?”

I hope you get something helpful from our conversation! It’s essential that we share our questions, doubts, struggles and challenges in order to discover that we’re not alone, and to provide support for our colleagues, ultimately affecting the mental health of the whole industry, and assisting small businesses in their important community-building work. (Another passion project of mine — come see me present the panel “Vulnerability as a Strength” at Bridging the Gap this July!)

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.

Tax season is over. Take a deep breath – whether you’re a bookkeeper or tax preparer, you’ve endured plenty of stress these past months, and now you’re in the perfect space between vacation and conference season to look back and figure out how to make it go better next year.

That’s what we do in our firm, anyway; I learned an amazing lesson from one of my favorite instructors, Tom Gorczynski, to plan for next tax season while the pain is still fresh in your mind! We schedule a company-wide zoom meeting, and everyone fills out a survey beforehand that asks about what worked, what didn’t, what they’d like to see go differently, who their favorite and least-favorite clients are, and why. This helps us incrementally improve year-over-year, and makes sure everyone has a voice. Then we send out cocktail kits and snacks to everyone, we celebrate, and we brainstorm. We even vote clients “off the island” together.

One of the themes that comes up every year is the need to move more clients off QuickBooks Desktop and onto QuickBooks Online. I know, groan… yet another talking head telling you to make the shift! At this point you’ve been bombarded with information on all the benefits of moving to QBO, so I won’t bore you with those. I’ll just share my own experience.

It was becoming more and more of a drag to coordinate with Desktop clients to review their books, and the new subscription structure made it confusing and frustrating to know who was on which version and how to make the most of what they were paying for. And of course, there were constant client fears around Intuit’s messaging, worrying they were going to stop supporting their product. But the biggest stressor for us was that it was actually getting hard to find junior bookkeepers who had ever worked with the Desktop program. (No joke. How about that for making a certain dancing accountant feel old?)

I assure you, I absolutely *hated* QBO for years; it was a clunky beast that didn’t have some of the most basic functionality that Desktop did – and I’m not just talking about the early days; this went on far too long and alienated many users. And while I held out for ages in moving to QBO, especially for certain types of clients that really benefited from what QBDT had to offer, I finally realized that it’s gotten to the point where the features I love about the Online version far outweigh its negatives. Between the concerted effort that Ted Callahan, Jessica McCracken and their team have made to actually listen to our community and implement some of the most-loved features; the fact that most third-party apps and tools no longer work with Desktop; and the advent of RightTool, an amazing browser extension by industry superstar Hector Garcia that supercharges what QBO has to offer… it’s time. It’s really time. QBO is now light-years ahead of almost anything that QBDT can do.

The point of outlining all this isn’t to convince you that you should migrate your remaining Desktop clients to QBO. It’s to suggest that when you do – follow my lead, and use exactly these reasons in your messaging. This became our mantra for communicating the value of converting, and it worked; at this point we only have one client left who needs to make the shift.

Think about it: your clients and your team members trust you, more than anyone else, to make smart and thoughtful decisions with everyone’s well-being in mind. If you convey the messaging that QBO is listening to us and responding to our requests, that RightTool will make you more efficient, and third-party apps will serve your clients’ needs better than the previous solutions, they will believe you, you’ll get buy-in, and in our experience, we found that clients were overwhelmingly positive and enthusiastic (though understandably still nervous) about the change.

Once you’ve got buy-in, it’s a simple matter of following some practical tips and advice to make sure the execution is done well.

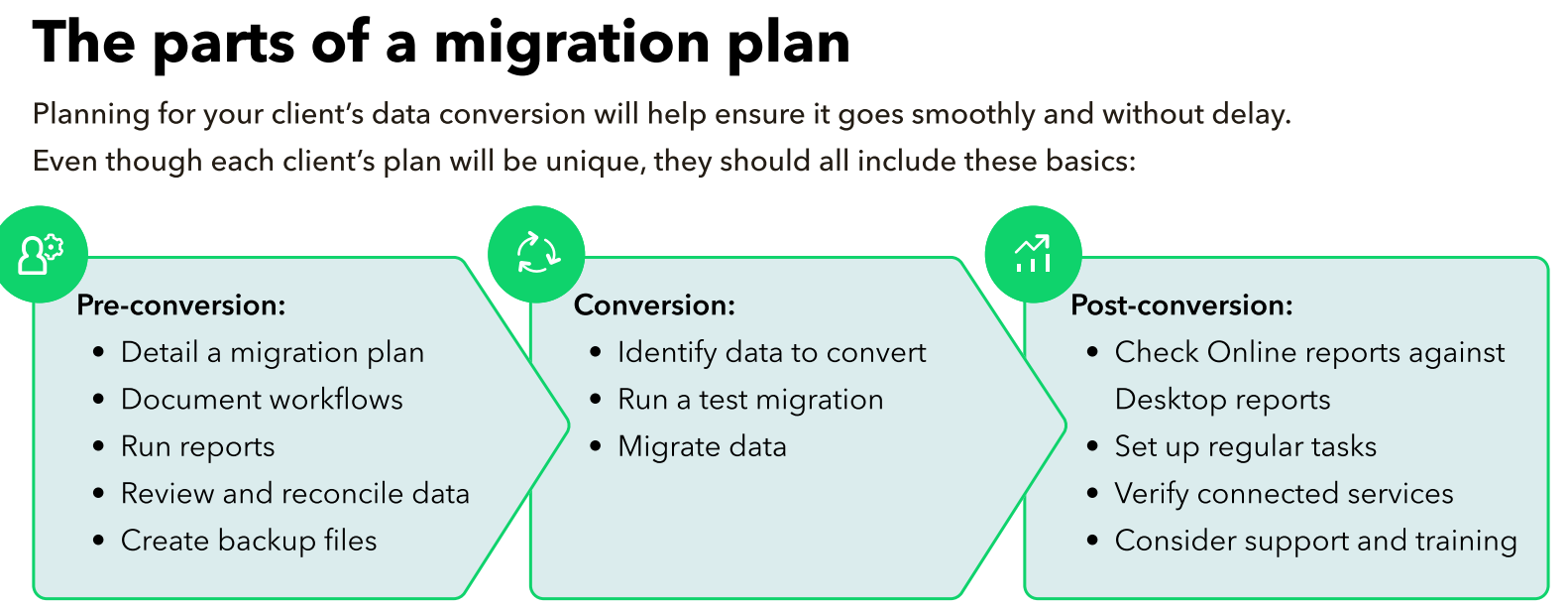

Understand the Conversion Process Intuit came out with a free conversion tool a few years ago that they keep tweaking to make it better; the most recent improvements announced at last year’s QB Connect blew me away – you can now batch migrate clients, meaning “do a ton at once and be done with it”. To be honest, it kind of made me wish I had waited to convert some of ours! However, as straightforward as they make it to migrate data from QBD to QBO, you do have to ensure your QBDT file is ready for the transition. This means backing up, running a verification on the file, ensuring it’s under the maximum target limit, and cleaning up any weirdo issues that have been hiding or buried for years, especially if you don’t regularly do a verification and rebuild. And most importantly, reviewing your “all dates” financial statements beforehand, exporting them, and comparing the same reports afterwards is essential.

Technical Resources for Conversion

I mentioned Intuit’s Conversion Tool, which guides you through the process step-by-step; they also have a QuickBooks Conversion Toolkit with checklists, webinar links, guides, client materials, and even a link to book a call to have Intuit do the conversion for you – just head here and then click on the “How to migrate” button to download the toolkit or set up a call. If you prefer your info from a third-party source, Hector Garcia does a short walkthrough on his YouTube channel, and Alicia Katz-Pollock is offering an Earmark webinar on May 21st. And if you have any concerns whatsoever about the process, consider outsourcing the job. We worked with CMB Hero and had a good experience, and I know DL & Associates does migrations as well; there are probably hundreds of companies or even trusted colleagues who’ve gone through the process before and can help you make sure it goes smoothly.

Research Third-Party Apps Before Converting

There are some super-fabulous apps out there that we love to use for syncing daily Point of Sale data, such as Synder, Bookkeep, and Shogo. But you need to look at the client’s needs and determine how they’ll be met in the new QBO world before making the shift – not all sync programs work with all POS platforms. Do demos, consult with colleagues, and figure out the timeline for implementing – in other words, not only the migration of QBDT data to QBO, but setting up the new system to work with the POS and get it all running. Our experience has been that some up-front planning saves loads of effort on the far end (which is when you’re pressed for time so the client can get back up-and-running).

Prepare Desktop Clients For The Change

And sticking with the theme of up-front planning… a little client hand-holding goes a long way. What they’re looking for is to follow your lead as their trusted advisor. The more you can compare and contrast their existing workflows and procedures with the new system, the more comfortable they’ll be with your proposal to move to QBO. Ideally, you already have Standard Operating Procedures in place for each of your clients. I wince as I type this, because I get that this is the “ideal” and not necessarily your reality – in all honesty, we’re still in the process of making sure each client has clear and detailed SOPs for every scenario. But this is a golden opportunity. Your instructions – in Word, an Excel checklist, Loom videos, or a project management app like Keeper, Financial Cents, or Asana – will build trust, making it much easier for you to illustrate to the client that this is a manageable change and that you’ve anticipated their needs. Side bonus: way less stress when a client (or your firm) loses a trusted team member and a new one needs to be trained ASAP.

To illustrate: in going through all the steps that a client’s office manager would complete each month as part of her billing process, and reproducing/ rewriting them using QBO, I noticed that she would no longer be able to run a particular report – at this point I had to decide whether we would come up with a different way for her to perform the same task, or whether we would track the data with a different feature in QBO so that she could run the report she was used to. Both approaches were fair; but the point is that I wouldn’t have noticed this change without walking through the process of retooling the procedures. This built trust with the client and made them more open-minded about making the change, because they knew we were actively anticipating and removing any stumbling blocks.

Client & Staff Training and Familiarization

As you know, transitioning to QBO doesn’t just involve moving data; it’s also about adapting to a new user environment. You’ll want to invest time in training sessions provided by Intuit or certified trainers like Royalwise (my personal favorite – I’ve been studying from Alicia for as long as I can remember). Intuit also offers an ongoing monthly session called QBO In The Know, which I encourage all my team members to attend as part of their paid training hours – this ensures that you don’t just get up-to-date, but that you stay that way, as the QBO ecosystem is constantly improving and new features are released every month. Hector Garcia’s YouTube channel is an endless wealth of information (I once hired a senior accountant with no degree and no certification based on the fact that she learned QBO by watching every single one of his videos. She’s now our Senior Accountant). Lastly, remember that QBO has a demo company! It’s a sandbox – have at it, and let your team practice without the risk of affecting real data.

Start by getting your client and team members’ buy-in. Take advantage of the available resources, and invest in training. With communication and planning, both your firm’s and your clients’ bookkeeping experience will end up better than it was with Desktop – we don’t have a single client that regrets having migrated, despite the fact that we all miss this-or-that feature (everyone’s got their favorite). But I promise it will be replaced by a new favorite. Remember, the goal is not just to convert data, but to enhance the overall efficiency and effectiveness of your accounting practices and those of your clients.

So… take that deep breath, plan for the future, and enjoy the heck out of that moment next tax season when you hear someone go, “oh wow, this really is so much better than it used to be!”

Note! As my readers know, I am downright fanatical about transparency and full disclosure (often to my detriment, as you may have noticed that I have a wildly popular award-winning blog that is non-monetized). Though this particular post is a paid partnership with Intuit, I want you to know that a) I wanted to write an article on QBDT–>QBO conversions anyway, but couldn’t find the time; getting paid allowed me the break from client work I needed to make it happen; and b) they didn’t delete a single thing when I presented it. In fact, they were totally cool with all my Intuit-bashing… which made me pretty impressed with them, to be honest. That’s twice now — let’s see if they go for a three-fer!

For years, we have stressed the importance to our clients of making quarterly estimated tax payments. And unlike many tax preparers, we also do bookkeeping, accounting, and consulting for our small business owners — so we’ve also encouraged them to have us do a quarter-by-quarter calculation of how much to pay.

There were many reasons for this: · Making sure the client had their books up-to-date and reconciled for the quarter, so they can be used for real-time managerial decisions; · Matching the cash flow of a given quarter (or the actual sales and vendor invoices, for accrual-basis clients) to the related tax liability; · Preventing the common situation of getting to tax-time and having a huge refund or balance due.

However, times have changed. We still want folks to make quarterly payments (see my related IRS & Illinois posts for how to do it online), but for the first quarter, at least, we’re asking everyone to use “safe-harbor” calculations.

Why Use 1Q Safe-Harbor Calculations Instead of Annualizing?

For one, the immense number of changes to our tax code since the Tax Cuts & Jobs Act (TCJA) took effect in 2018 has made tax planning substantially more complex than it used to be. The amount of time it takes to do a “back of the envelope” or “paper napkin” calculation has tripled. (And in case you’re curious — we use tax software and Excel, not used envelopes and paper napkins in our firm. That’s how you know you’re working with a real professional.) Both the effort involved and the cost to the client have increased accordingly.

Relatedly, first-quarter estimated tax payments are due on the same day as personal 1040 and C-Corp 1120 taxes are due. And since our tax-time work is a deeper dive than it used to be, and the estimated tax calculations are more complex as well, there simply isn’t enough time to do a full-on calculation for each and every client that requests it — at least, not if we also want to be well-rested and in good health, so we can do our very best on the remaining annual tax returns.

There’s good news, too, however — the state of Illinois — and many other states, used legislation to create a loophole for getting around a pesky TCJA limitation on the State And Local Tax (SALT) deduction. I won’t explain it all here, but the result is that all of our S-Corp and Partnership (aka “Pass-Through Entity”, or PTE) clients are paying their personal state taxes through the company. This is a very easy and predictable calculation, as Illinois charges a flat tax (not socially progressive, but it certainly is simple) and requires the annual liability to be divided by four and paid evenly across the quarterly deadlines.

(Side note: the deadlines are not actually quarterly. Due to the timing of the federal government’s fiscal year-end and individuals’ calendar year-end, they are skewed such that they’re not even the same number of months per quarter. You would think that of all the government departments that could count properly, it’d be the IRS, but apparently not. The due dates are 4/15, 6/15, 9/15 and 1/15 — though many are better off making the final state tax payment by 12/31.)

As a result, quarterly calculations for the state simply aren’t necessary for the first quarter (possibly even the first three quarters, depending). Given that the states seem to live for assessing penalties and interest for underpayment of estimated taxes (they are wildly aggressive about it), this is the best approach to take.

But it’s not just the states that issue penalties and interest for underpayment of taxes — the IRS does, as well. Much less aggressively, however, and they do still have the notion (that the new Illinois PTE tax law does not) of “annualizing” your quarterly taxes. This means that you presume the amount you made year-to-date is representative of the whole year, and paying quarterly tax based on that projection. It works great for small business owners who have lower income in the first three-quarters of the year and then make most of their profit in the final quarter.

Just to be clear: we still do this for our clients… but we wait until the second or third quarter, and in some unusual cases, we wait until November and then do a thorough analysis of the year thus far. It’s just that there’s little point in running these calculations for the first quarter anymore — it’s almost never representative of the rest of the year, and it places them into a precarious situation where they may end up underpaying by too much and then owing penalties and interest. Or, at the very least, having to pay us at tax-time to fill out the complicated annualization schedule on the tax return. If you want to be more accurate with your calculation, because you expect your income to be substantially higher or lower than last year, then ask to book a May tax-planning session to get squared-up for the 2Q payment, due June 15.

Last, but not least — we’ve decided to have all our clients commit to a monthly bookkeeping and accounting contract with us. Doing annual clean-ups during tax season simply is no longer sustainable (to be honest I’m not sure it ever was, which is one of many reasons so many CPAs are burned out), and isn’t cost-effective. It’s also not fair to our other clients — who are on a monthly schedule — to have to wait in line while we work on those who swing through just once-a-year. And most importantly, we truly believe that all small business owners should be looking at their financial statements regularly to help them make impactful decisions throughout the year — ones that can sometimes be the difference between turning a profit or enduring a loss. And since everyone will be on a monthly schedule, the motivation no longer exists to do quarterly reviews for estimated tax purposes, purely as a way to get clients motivated to catch up on their books.

Where To Find Your Safe-Harbor Amounts and How To Pay Them

If you’re a client of ours, or of pretty much any tax professional out there, calculating safe-harbor quarterly estimates can and should be a part of preparing your annual tax return.

After reviewing and signing your return, your CPA (or EA, JD or non-credentialed preparer) will e-file it, and once it’s accepted by the IRS and state agencies, they will either send over vouchers (which I wouldn’t bother using, because we want to pay taxes online almost every time that’s an option), or a list of required payments — whether that’s in a letter or a little chart form where you can check ’em off. However you get them — put them in your calendar now. Do not rely on your tax preparer to remind you. This is not their job. You are a grown person running your own business, surrounded by technology that is designed for precisely this kind of thing.

And if you’re in a panic and can’t find the amounts, the general rule is that you want to pay 1/4th-ish of your total tax liability for the prior year (a bit higher for some states, such as Illinois). Again, if we do your taxes, you should have already received these totals for 2024, or will be receiving them as soon as your return is finalized.

Frequently Asked Questions

1) What if I have an extension? Two options here: a) provide your tax preparer all the docs you already have and ask them to do their best to give you an estimate; they can even add that to the amount you’ll need to pay with an extension — which means if your extension payment estimate is short, the 1Q estimate will make up the difference, and either way, you’ll just apply the balance to the current tax year; or, b) go ahead and keep paying the same amount you paid for last year’s quarterly taxes; some payment is better than none.

2) What if I don’t have a tax preparer? All the DIY tax programs out there can do this, too — they’re not very helpful for the tax planning that we do with our clients for 2Q & 3Q, and certainly not for 4Q — but they do a perfectly fine job with safe-harbor estimates. Alternatively, check out my colleague Hannah Smolinski‘s great YouTube primer on how to calculate estimated taxes.

And since you asked, here’s a fabulous photo of Hannah and me at QuickBooks ConnectFest.

3) What if I can’t afford to pay my quarterly estimates? Pro tip: Did you know you can break your quarterly payment into smaller chunks? Let’s say you owe $2400 per quarter and you’re worried that you won’t have enough set aside by the time the due date arrives, because it’s so hard not to raid your own savings account when opportunities call. Just go online and pay $800 per month instead. Or $200 per week. It gets tricky with the weird quarterly tax due dates, but you are a smart cookie and can figure out the math. The point is that you don’t have to save it all up and then make the payment. If you have cash on hand, you can go in there now and do it while it’s on your mind, even if it’s a partial payment. Something is better than nothing.

4) What if I forgot to pay for a quarter? Go in there and make a payment now. The penalties are per day, so the sooner you make up the difference the better.

5) What if I have additional questions about the process? Throw whatever you can at the quarterly estimates and contact a CPA to help you… after Tax Day. Please be respectful of the plight of tax preparers right now. It will not serve you long-term to try to wedge yourself onto someone’s calendar last-minute: almost all the good ones had a deadline for submitting tax materials weeks ago; we’re all exhausted and likely to make mistakes this time of year if we’re taking on too much and not taking care of ourselves; and you want to start off on a good foot when building a relationship with a trusted advisor. The amount of penalties and interest that will be due if you underpay slightly is not that significant if you’re going to be making up the difference in a month, so just pay what you can and get on-track later.

Now, get yourself online and go make those first-quarter safe-harbor quarterly tax payments, already!

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.

The IRS is offering an amazing deal to those who either fraudulently or mistakenly claimed Employee Retention Credits (ERC) to which they weren’t entitled.

If a taxpayer claimed and received ERC funds, and for whatever reason now realizes that they may not actually have qualified (either for a particular period or for the whole thing) — they can return 80% of the money to the IRS and call it a day.

Considering that more than 3.6 million claims have been submitted, and the IRS refunds run up to $26,000 per employee… we’re talking about big dollars here. As of July 31, 2023, the IRS Criminal Investigation division had initiated 252 investigations involving over $2.8 billion of potentially fraudulent ERC claims.

We were extremely diligent in filing ERC claims for our clients — it took literally months of effort in research, software development, calculations, data collection, interviews and narrative-writing, not to mention preparing the actual tax forms and support. So initially I was extremely frustrated to find that people who filed claims without substantiation could return only 80% of the money and keep 20% for themselves. However, IRS Commissioner Werfel explained the rationale behind this decision, as reported by Journal of Accountancy:

“We could not stand idly by as small businesses were being taken advantage of by promoters trying to get hefty fees,” he said. He later described the 80% figure as “an important incentive to participate in the disclosure program. Participating businesses do not need to repay all 100% of the payment they receive.”

And this makes sense. Not just our clients, but our own firm (which decidedly does not qualify for ERC) was bombarded by calls and official-looking forms designed to lure us in to thinking that we were entitled to this “free money”. And they charged exorbitant fees in the 20-30% range, without providing any of the substantiation a taxpayer would need in case of audit. As a result, these scams topped the list of the IRS “Dirty Dozen” in 2023.

So it’s not surprising that, although the process to participate in the voluntary disclosure program is quite easy and simple — one of the requirements is that the applicant must provide names, addresses, and phone numbers of any advisers or tax preparers who helped with the claim, as well as details about the services provided. I’m hoping that this will cause some of these “mills” to get what they deserve for defrauding small businesses and our government.

Taxpayers wishing to participate in the ERC voluntary disclosure program must notify the IRS by completing and submitting Form 15434, Application for Employee Retention Credit Voluntary Disclosure Program. Program participants will not be charged underpayment interest, and the IRS will not assert civil penalties against them for underpayment of employment tax attributable to the ERC. And those that cannot repay the required 80% might be considered for an installment agreement.

If you are among those who has submitted a claim that hasn’t been approved yet (or received your checks but have not yet cashed them), you can still withdraw your claim, following instructions on the IRS ERC FAQ (#5 under “Correcting an ERC Claim”). They even include a sample withdrawal form.

I’ve interviewed countless ERC claim companies and narrowed it down to only two with whom I have trusted my colleagues and their clients. (It’s truly stunning how many out there have no idea what they’re doing, even the ones that aren’t intentionally skirting the rules.) One of them, Tri-Merit, recently released an episode of Randy Crabtree’s Unique CPA Podcast that dives into the biggest ERC changes for 2024. The service of theirs I recommend the most often (for which I can offer a referral link) is their “ERC Verification” offering, where they take a look at what you’ve claimed and either verify that it was done correctly, or recommend changes and help process the amendments. They stress that it is never too late to fix a claim that has already been paid.

And for those of you who have filed accurate ERC claims and are still waiting for the IRS to end its moratorium — still no information on when processing will begin again. Keep your eye on the AICPA’s ERC Resource Center; or check in with my blog — I’ll be one of the first to joyfully report it when the time comes!

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.

Thanks so much to Insightful Accountant — a leader in news and education for our industry — for inviting me to join a truly exceptional group of colleagues on the inaugural advisory panel.

“The primary purpose of the panel is to help us stay in touch with the audience we serve and to continue to provide the content you want. The panel members will also be instrumental in helping us shape the future of Insightful Accountant by identifying areas of improvement, new opportunities and being a collective sounding board for us as we explore what is next for our business.“

I’m looking forward to getting to know some new friends and reconnecting with old ones… and most importantly, helping shape a future for Insightful Accountant that addresses the needs of our industry. It’s through these connections that we can truly understand and address the evolving needs of accountants, bookkeepers, tax preparers, advisors, apps and vendors, and of course — the small businesses that we serve.

Read more about the rockstars on this year’s panel here!

And if you’re a member of our community, please reach out and let me know what you find valuable about the content, education, and opportunities Insightful Accountant affords you, as well as what you’d like to see improve.

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.

QB Ledger was announced at QB Connect a few months ago.

If you’re like me, March is that special month from hell where clients that have ignored your pleas for four quarters in a row suddenly show up again… and lucky you. Because now they’ve got a new AirBnb rental property in tow! Or yet another side gig! Or even better: an estate that they have to manage until it settles, and it’s caught up in probate!

To be honest, I’ve been slowly weeding these folks out of our client list – and I feel like a jerk about it – but it just doesn’t make sense for us to spend time during our busiest season getting them caught up on a year’s worth of transactions. Especially because these are the same characters that tend to be super price-conscious, and are somehow convinced that because they have a low volume of transactions, they shouldn’t have to pay for the monthly QuickBooks Online subscription – “can’t you just use our bank statements or a spreadsheet?”

For anyone reading this who isn’t intimately familiar with these classic dance moves already – no, we can’t just use bank statements or a spreadsheet. There’s no double-entry bookkeeping, no debits and credits, no Balance Sheet, and far too many potential lurking mysteries to be uncovered only after all the manual data entry is already complete. At some point we put a stop to these shenanigans… only to find ourselves sitting in QB Desktop, doing all the write-up work on behalf of our clients – a total reconstruction job. More reliable, but not less effort. (And moot at this point, since QB Desktop has gone subscription and is slowly asphyxiating.) And yet – I was a tiny startup at one point, too! I get not wanting to spend big bucks on a full-featured bookkeeping package for an activity that’s not earning much money.

By this point we’ve filtered out most of these types of clients, raising our minimum to price out some of the potential clients we really did (in theory) want to help – itty bitty start-ups or serial entrepreneurs, those that can’t resist a good deal on real estate, or people who sadly lost a loved one and are adrift as to how to handle the demands of bookkeeping for the estate. (I did this for both of my grandmothers back in the day, using my accountant’s copy of QuickBooks Desktop. It was not fun, but boy was my family relieved that they had a knowledgeable QB ProAdvisor handy.) But some remained. Clients who we really like who have been with us for ages, or who have another full-on business that we support, or whose side-gig really serves our community and they deserve a break.

(You read the title, right? I mean… you can see where this is going?)

Those who know me know that I don’t mince words about Intuit as a company. They’ve created a core product that I love, which I’ve been using in some form or another since 1993 (oof, that dates me) – but when they cross me (and they do, more than I’d like), I call ‘em out on it. I don’t like the constant price increases (though I do see the constant improvements), nor the aggressive marketing of corollary products to us and to our clients. I don’t understand why they haven’t fixed some basic functionalities we’ve been asking about for literally years. But the only reason I bother complaining is that I truly believe in QuickBooks products, and the ecosystem they’ve built, and that other software companies have built around them. Which is why it was delightful to be there when QB Ledger was announced at QB Connect in November (see photo above), and all the more delightful that since then, I’ve been able to honestly say I’m in love with this new product.

Why? What’s the hype?

Nothing. There’s no hype. That’s what’s so great about it. It’s just plain old reliable QB Online that we know and love, but without all the bells and whistles, and therefore totally affordable for uncomplicated files. It basically strips down the system to the core functionalities but retains the tools that are the most timesaving. And therefore, they only charge you for the basics. It’s $10/month per client.

At this price, and with the connected bank feeds, rules and reconciliation features, we can blow through an entire year of transactions on a cash-basis filer in literally a couple hours, and still make it affordable for the client, while maintaining plump margin for our firm. Since the bank and credit cards are connected, we don’t have to rely on the client for statements before we get started, so we can take care of most of the work well before tax-season begins. In most cases, the client won’t ever need access to the system, because it’s not about managerial insights and analytics – it’s just a compliance engagement that gets us to the point where we can file an accurate return. But unlike QB Self-Employed, this is real accounting software that gives us double-entry accounting, adjusting journal entries, and spits out proper financial statements. And also unlike QBSE, it allows for a full-on easy upgrade should the side-hustle turn into a more full-fledged business, or the real estate toe-dipper turns full-on house-flipper. (And yes, two accountants can be connected, just like the other QBO products, so if you’re not doing CAS and tax in-house like us, you can have a bookkeeper firm and tax prep firm both connected.)

Things to know before you dive in: – It seems like QB Support staff haven’t all been trained yet on what it can and can’t do, how many and which types of users can be attached, and which use-cases make the most sense, so be aware of that. It’s also sometimes tricky to get the client added (to set up the bank feeds) because the accountant user gets assigned both as accountant and admin; as with other versions, when this happens it can bea pain to switch that over to the client. So, make sure not to check the box to make yourself primary admin when setting it up. – And… they’ve got a weirdo situation where you can’t use a Customer name anywhere in the file (presumably they deactivated this because there’s no invoicing, which is fine… but we still need that field). I’ve got it on good authority that this isn’t a bug. I suspect this was done with the expectation that those who have customer reporting needs will just upgrade, but I don’t personally think that it will serve the purpose of moving them to Simple Start. They’ll just use an external invoicing or scheduling program to track income by customer instead of upgrading – especially because those third-party apps do in fact create these customers in the app – and then they’ll be hooked on that invoicing feature… instead of tracking things by customer in QB Ledger and eventually upgrading to Simple Start. I have clients in all walks of QBO and there are startups that can’t initially afford Simple Start who will eventually get there… but they’re going to need customers to make that happen. Another workaround: some folks are using the Vendor field with a “-Cust” after the name to get around this. – And lastly, bummer – you can’t downgrade, you can only start a new QB Ledger file or upgrade that file. (Yeah, they were thinking about all the reluctant clients who we had to talk into paying for Simple Start that don’t actually need A/R and A/P and would be fine on Ledger… really wishing they’d released this version years ago.)

Hector Garcia just released a half-hour complete tutorial on QB Ledger for accountants and bookkeepers, so if you want a deep dive on the specifics, then you’ve found your instructor.

Start-ups, trusts, estates, once-a-year write-up or tax prep clients, small side-hustles, AirBnB and other rentals, your glam diva marching band (ok, maybe my glam diva marching band)… the list goes on. Intuit has finally taken the core functionalities that are the reason we celebrate QuickBooks Online, and packaged them into an affordable option. It’s earning them goodwill, providing a pipeline for future upgrading customers, and will surely make the switch from Desktop to Online more attractive for the masses. For us, it fits seamlessly into our strategy to shift away from once-a-year rush work. For bookkeepers just getting their start, it allows them to take on small freelance and hustle clients. Welcome to the QB family, Ledger! We’re glad you’re here.

(What’s that, you want to learn more about QB Ledger? I knew you were gonna want to know how – so I’ve conveniently set it up for you to check out this page here.)

Note! As my readers know, I am downright fanatical about transparency and full disclosure (often to my detriment, as you may have noticed that I have a wildly popular award-winning blog that is non-monetized). Though this particular post is a paid partnership with Intuit, I want you to know that a) I wanted to write an article on QB Ledger anyway, but couldn’t find the time; getting paid allowed me the break from client work I needed to make it happen; and b) they didn’t edit a single thing when I presented it. In fact, they were totally cool with all my Intuit-bashing… which made me pretty impressed with them, to be honest. I might just do this again sometime. We’ll see.

I first came across the concept of “Open Book” management (OBM) for restaurants back in 2009, when I purchased Zingerman’s Guide to Good Eating from a local food & wine retail client of mine and we were discussing their recent adoption of this business philosophy — first popularized by Jack Stack in his excellent 1992 book, The Great Game of Business. Having lived in Ann Arbor for 10 years and attended the University of Michigan, I was of course a fan of their world market and pricey-but-delicious deli salads and sandwiches. But it wasn’t until 2012, when I took a deep dive into restaurant accounting and attended a series of seminars by the former Restaurant Seminar Institute, that I made the deeper connection between healthy financial communication and healthy small businesses. The class instructor had referenced various approaches to management, and included OBM among others on the list. A year later, I began working with local restaurant Honey Butter Fried Chicken — whose owners, as it turns out, had taken Zingerman’s OBM course and were in the process of implementing it in their fledgling project.

I spent the next few years working with them as they fine-tuned their metrics, delivery, and compensation structures, as well as trained their managers and the rest of the staff on why any of it mattered. First-hand, the benefits of this transformative approach were made apparent, and I became an eager proponent of OBM. Later, as I began to specialize in co-ops, I saw the same lessons filtered through a lens of cooperative management and policy governance that in some cases fit nicely with the OBM framework (though not always — check out this excellent Columinate article on lessons learned the hard way; an illuminating quote: “Getting the responsibility into the hands of the staff each week is an important transition in making it successful. Yet, many times, we see managers hanging on to the reporting lines for too long, which leads to disengagement and disinterest on the part of the staff. They won’t learn it or care about it until they are responsible for it”).

So imagine my delight when I read this month’s Plate online magazine and saw that my former clients are participating in a free webinar on Open Book Management — and how to determine whether it’s a fit for your restaurant! From PlateTalks: “These owners will talk about what it takes to get your books in order, how they share key data points with their teams, and what their staff has gained from the model.”

According to Zingerman’s — and this lines up with my personal experience — OBM can lead to better results: but more importantly, it lines up with the values of many small business owners. Side benefits include building commitment, better business decision-making, and teaching everyone to think like an owner.

Open Book Management isn’t something that can be implemented in a silo, however — a concept summarized well in a case study by the non-profit International Council on Hotel, Restaurant, and Institutional Education (CHRIE), “…small to medium enterprises can greatly benefit from open book management, the creation of a strong and qualitative mission statement, and a cohesive organizational culture that blends well with the external macro culture. Any one of these elements appears to be dependent upon another. For example, Zingerman’s, or any other company could have an open book management style of operation – but without a clear mission, the company would not do as well in the marketplace. Zingerman’s could have a great organizational culture, but without open book management, employees would not take ownership of their jobs, and therefore the bottom line would suffer.”

There are loads of articles and courses out there on Open Book Management — and plenty of restauranteurs who are glad to network and share their experiences. For a short introduction, I encourage you to check out Josh and Christine and their colleagues, as well as the folks at Plate, on March 5, 2024 from 1-2 pm Central. This is not a referral link — I’m just excited to get the word out, to help as many small business restaurants as I can in my time. I’ve always maintained — and as our mission goes — we believe the vibrancy and character of our neighborhood depends on thriving small businesses lending their unique vision to our communities.

If this or any other posts on the website were useful to you, and your financial situation permits it, please consider contributing to my tip jar. Ths allows me to continue to provide free accounting resources to small businesses who do not have the funds available to hire a CPA.

If you’re a regular reader, you already know that I’m a huge fan of the National Association of Tax Professionals (NATP), for a bunch of reasons:

Fabulous and affordable education with top-notch instructors

Straightforward “how-to” resources

Practical monthly newsletter with case-studies

On-demand “pay as you go” research service

And a very fun group of folks at the annual conference! (That last one’s a teaser for the final photo in this post.)

I’m especially indebted to NATP because when I first started doing taxes, I wasn’t a CPA yet — and spoiler alert: they don’t really teach you that much about tax preparation when studying for your CPA exams; in fact, three-quarters of the test aren’t related to taxes at all. In those early days, NATP education was the best-quality, most affordable that I could find without being a member of AICPA. (And I tried *all* the groups out, to be clear.)

Anyway, point here is that not only do you not have to be a CPA or EA to take and benefit from their classes — in fact, you don’t even have to be a tax preparer. I am a passionate proponent of teaching bookkeepers what they need to know about taxes to be better at their jobs, coordinate and communicate effectively with their clients’ tax preparers, and level-up by providing value-added advisory services to their clients.

To that end, here’s an upcoming NATP webinar that I suspect will be pretty dang useful for anyone doing client accounting work — bookkeeping, tax, advisory, CAS, and so on. You don’t even have to be a member to attend.

I get a lot of questions and see a great deal of misinformation out there about entity choice… here’s an opportunity to learn more about how to help your clients decide which entity structure is the best choice for them.

(Note: this is *not* a referral link — I’m just really excited about this education getting out there into the world. The presenter, Larry Pon, is a great guy and super-knowledgeable about all the ins-and-outs of this topic.)

From NATP:

Proficient knowledge in selecting the optimal entity structure is vital as it directly shapes a business’s tax outcomes. Strategic choices can enhance deductions, reduce liabilities and ensure regulatory compliance, contributing significantly to a business’s financial well-being and long-term success.

We know you want the best for your clients, so we want to arm you with the knowledge to do so.

As clients start new businesses, one of the major decisions to make is what entity type is best for them? Limited liability companies are by far the most commonly selected type, but did you know, the IRS doesn’t recognize LLCs as an official entity? LLCs can default to a disregarded entity or a partnership depending on the number of members they have, or they can select S or C corporation status.